[ad_1]

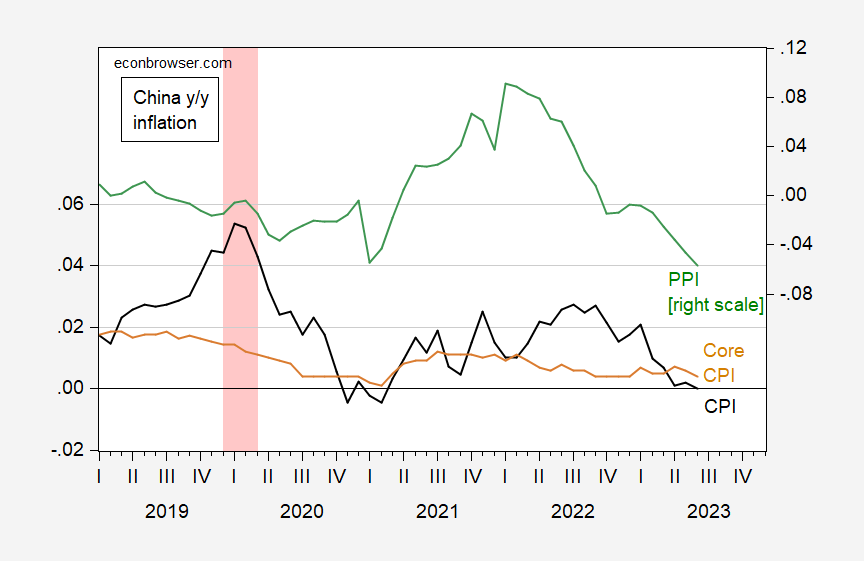

The June numbers for Chinese language inflation stunned on the draw back: 0.0% headline vs. +0.2% y/y Bloomberg consensus, -5.4% PPI vs. -5.0% consensus.

The value stage is proven in Determine 1, and year-on-year inflation in Determine 2:

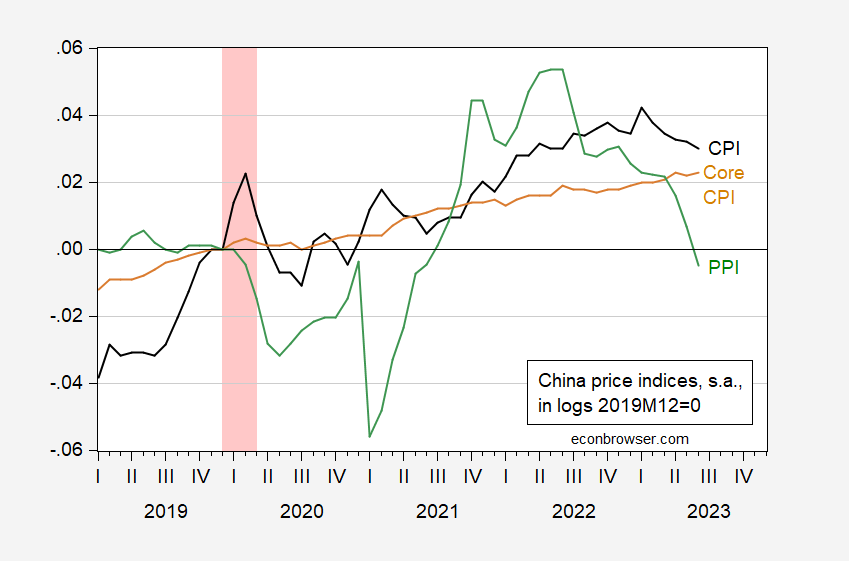

Determine 1: China CPI (black), core CPI (tan), and PPI (inexperienced), all in logs, 2019M12=0. ECRI outlined peak-to-trough recession dates shaded pink. Supply: Kose/Ohnsorge – World Financial institution and IMF, IFS, each up to date utilizing TradingEconomics; and writer’s calculations.

Determine 2: China year-on-year inflation fee for CPI (black), for core CPI (tan), and for PPI (inexperienced). ECRI outlined peak-to-trough recession dates shaded pink. Supply: Kose/Ohnsorge – World Financial institution and IMF, IFS, each up to date utilizing TradingEconomics; and writer’s calculations.

Why the anxiousness about deflation? Bloomberg notes that deflation will be taken as an indication of slowing financial exercise, an enormous fear given the less-than-anticipated rebound from the tip of the zero-Covid coverage regime. (In some preliminary regressions, I discover a 1 ppt output hole outlined utilizing a HP filter induces a 0.44 ppt greater inflation fee, after controlling for lagged inflation, over the 1990-2019 interval).

There’s additionally the truth that PPI inflation has continued into unfavorable territory. Whereas it’s tempting to conclude that declining PPI inflation will end in declining CPI inflation, the proof in help of this view is blended; Solar et al. (2021; additionally IJFE 2023). A Granger causality take a look at 2010-2019 signifies one can’t reject null that PPI m/m inflation doesn’t trigger CPI inflation, nor can one reject the null that CPI doesn’t trigger PPI at typical ranges. Then again, one can reject the null speculation that the PPI doesn’t trigger core CPI inflation on the 10% msl.

[ad_2]

Source_link