[ad_1]

At present we’re happy to current a visitor contribution by Jamel Saadaoui (College of Strasbourg). This publish relies on the paper coauthored with Valérie Mignon (College of Paris Nanterre).

Introduction

The final twenty years have been characterised by spectacular adjustments within the oil market on the international degree. Though the position of the Chinese language economic system within the oil market was negligible earlier than China’s entrance into the WTO, the state of affairs dramatically advanced afterward. Certainly, China has change into a major participant within the oil market, with 16.4% of world consumption in 2021. Turning to the US, it’s the first largest client (19.9% of world oil consumption) and producer (16.8% of world oil manufacturing). Given the burden of those two nations, the evolution of their political relationships might thus strongly have an effect on the dynamics of oil costs, along with geopolitical dangers.

This paper tackles this difficulty by investigating the affect of political tensions and geopolitical dangers on oil costs. Whereas varied articles have tried to seize these results utilizing proxy variables (Chen et al., 2016; Lee et al., 2017; Miao et al., 2017; Perifanis and Dagoumas, 2019; Abdel-Latif and El-Gamal, 2020; Qin et al., 2020; Caldara and Iacoviello, 2018), Cai et al. (2022) is the primary examine that depends on a quantitative measure of political relations to research their doable impacts on oil costs.

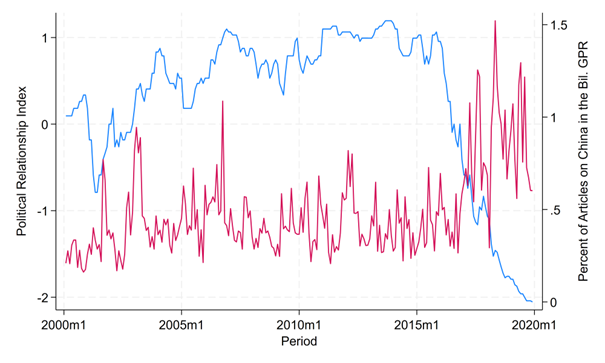

Within the current paper, we go additional than the earlier literature by counting on two complementary quantitative measures. First, we use an index constructed by the Institute of Worldwide Relations at Tsinghua College to measure political relationships for China and its main commerce companions (see Yan (2010) for a dialogue). This Political Relationship Index (hereafter PRI), ranging between -9 and 9, signifies whether or not the nations are rivals (between -9 and -6), in a tense relation (between -6 and -3), in a nasty relation (between -3 and 0), in a standard relation (between 0 and three), in good relation (between 3 and 6), and mates (between 6 and 9). PRI fluctuates based on a scale much like the Goldstein scale (Goldstein, 1992). Every month, dangerous or good occasions showing in Individuals’s Each day and on the Chinese language Ministry of International Affairs web site are included to replace the index. As proven in Determine 1, the US-China political relationships dramatically deteriorated after the start of Trump’s commerce warfare.

Second, we use the bilateral model particular to China of the Geopolitial Danger Index (hereafter GPR) launched by Caldara and Iacoviello (2018). GPR is a month-to-month index obtained by operating automated textual content searches on the digital archives of 11 newspapers that counts the proportion of articles associated to antagonistic geopolitical occasions (wars, terrorist assaults, tensions between nations, and so forth.). The bilateral model of GPR refers back to the proportion of articles in US newspapers coping with antagonistic geopolitical occasions that concern one particular nation, particularly China in our case. This bilateral index makes use of three US newspapers: The New York Instances, Chicago Tribune, and The Washington Submit. As proven in Determine 1, the proportion of articles related to China elevated considerably after Trump’s commerce warfare started.

Determine 1: Political Relationship Index (left-hand scale) and Geopolitical Danger Index (right-hand scale)

Notes: PRI (in blue) could be downloaded at: http://www.tuiir.tsinghua.edu.cn/imiren/data/1091/1320.htm, and the bilateral GPR (in pink) at: https://www.matteoiacoviello.com/gpr_country.htm. PRI is expressed as signal() ∗ (|| + 1) and ranges between -2.30 and a couple of.30: rival nations between -2.30 and -1.95, in a tense relation between -1.95 and -1.39, in a nasty relation between -1.39 and 0, in a standard relation between 0 and 1.39, in good relation between 1.39 and 1.95, and mates between 1.95 and a couple of.30. PRI, Political Relationship Index; GPR, Geopolitical Danger Index.

To be able to analyze the affect of the US-China political relations on the oil market, the bilateral GPR index particular to China and the PRI index could be seen as complement. Certainly, the bilateral GPR doesn’t give attention to the relation between the US and China, slightly it gives an total image of the geopolitical uncertainty for China. For instance, the Sino-Japanese dispute over the Diaoyu/Senkaku Islands may very well be included within the GPR index particular for China, however will probably be included within the Sino-Japanese PRI, not within the PRI for the relation between US and China. The PRI for the US and China is concentrated on the bilateral relationship. On this respect, we contribute to the literature on the macroeconomic penalties of geopolitical dangers (see Caldara and Iacoviello, 2022) by contemplating the bilateral political relationships between the US and China. We analyze the doable complementarities between the PRI and the GPR index.

Methodology and baseline outcomes

Utilizing month-to-month knowledge from January 2000 to December 2019, we run SVAR and LP analyses (Jordà, 2005) to guage how oil costs react to shocks on PRI and on the bilateral GPR index. We take into account the next variables within the SVAR mannequin: bilateral GPR for China (gpr_cn), oil provide (international oil manufacturing, million barrels/day, lpro), oil demand (OECD and 6 main non-member economies (Brazil, China, India, Indonesia, the Russian Federation, and South Africa) industrial manufacturing, ldem), oil costs (actual WTI spot value, lrpo), and PRI between China and the US (lpri_us), respectively. These oil-related variables are remodeled into pure logs. For PRI, we use the log-modulus transformation, which is outlined for zero and destructive values. All of the oil-related variables are taken from Christiane Baumesiter’s private web site (Baumeister and Hamilton, 2019). We use the identical variable ordering as in Cai et al. (2022)

Within the following, we are going to give attention to the baseline outcomes for the oil costs and on two particular geopolitical occasions, particularly (i) the US bombing of the Chinese language embassy in Belgrade and (ii) the 1989 Tiananmen Sq. occasions.

Unanticipated destructive shocks (deterioration of political relations) are extra frequent throughout Trump’s commerce warfare. Equally, we observe an increase within the frequency of sudden constructive shocks (a rise in articles associated to China in US newspapers) throughout the identical commerce warfare interval.

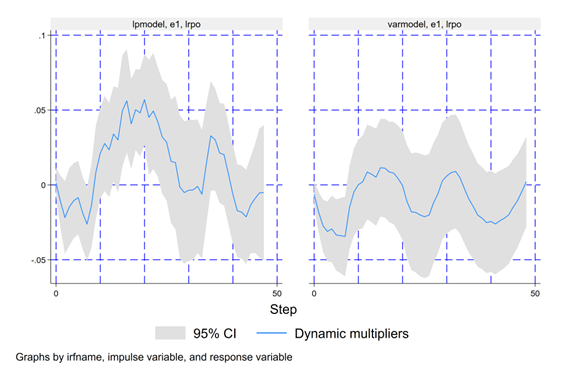

In Determine 2, the LP’s dynamic multipliers present that enhancing political relations positively impacts the true value of oil after 13 months; this constructive impact lasting about 10 months. Turning to the VAR’s dynamic multipliers, we observe (i) an preliminary drop that’s not important in LP, and (ii) the absence of a major constructive impact. General, LP appears to seize the short-run dynamics. These outcomes are slightly intuitive. An unanticipated enchancment in PRI for the US means a greater relationship between the 2 main gamers on the earth economic system and within the oil market. Optimistic shocks on PRI are thus linked to the demand aspect and are related to optimistic expectations relating to future financial exercise, driving up oil costs.

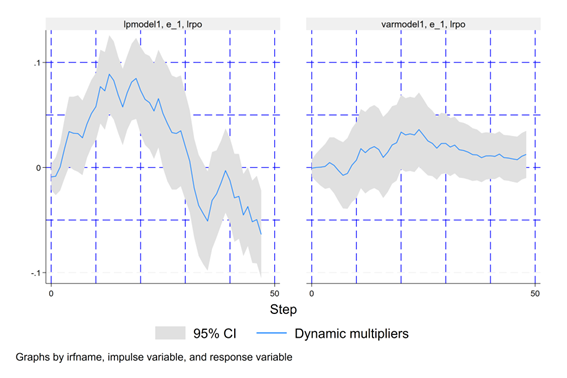

In Determine 3, we take into account the structural shocks in GPR for China. The LP’s dynamic multipliers outcomes are similar to these associated to PRI for the US. Certainly, we observe an increase in the true value of oil after 8 months. This improve lasts round 18 months and is of upper magnitude than the shocks on PRI for the US. Relating to the VAR’s dynamic multipliers, the rise isn’t important, as in Determine 2. Our outcome that greater geopolitical dangers drive up oil costs persistently is in keeping with the actual fact that there’s a tendency to confound all geopolitical tensions with oil provide shocks provoked by geopolitical tensions within the Center East (Caldara and Iacoviello, 2022). Optimistic shocks on GPR are thus linked to the provision aspect and replicate fears of oil provide disruption, pulling up oil costs.

Determine 2: Dynamic Multipliers for the Actual Value of Oil (Shock on PRI for the US)

Notes: Left graph: LP, proper graph: SVAR. As proven by Cai et al. (2022), the outcomes are strong to totally different orderings. The actual value of oil and the sequence of structural shocks on PRI for the US are uncorrelated. PRI, Political Relationship Index.

Determine 3: Dynamic Multipliers for the Actual Value of Oil (Shocks on GPR for China).

Notes: Left graph: LP, proper graph: SVAR. As proven by Cai et al. (2022), the outcomes are strong to totally different orderings. The actual value of oil and the sequence of structural shocks on GPR for China are uncorrelated. GPR, Geopolitical Danger Index.

US bombing of the Chinese language embassy in Belgrade

Within the following, we are going to run the identical analyses with samples from February 1990 after the 1989 Tiananmen Sq. Occasions, and from February 1985 the place the current GPR index is on the market. The outcomes are largely comparable, however they provide some proof concerning the complementarity between the GPR and PRI index within the understanding of the macroeconomic penalties of geopolitical threat. We begin with the pattern after the 1989 Tiananmen Sq. Occasions. The pattern begins now from January 1990. We’ll give attention to a selected occasion that has not been reported and perceived in the identical within the US and in China. Certainly, on Could 7, 1999, the Chinese language embassy in Belgrade was bombed by the US throughout the NATO bombing of Ex-Yugoslavia, as reported by Ponniah and Marinkovic (2019). As proven by Bondarenko et al. (2023), geopolitical dangers can’t be universally measured. In a case examine on Russia, they present that geopolitical threat shocks recognized from English-language information sources shouldn’t have any affect on the Russian economic system, whereas Russian-language information sources do have an effect on the Russian economic system.

This big destructive shock can solely be seen within the PRI index. This essential destructive occasion has not been reported in the identical approach within the US press (Parsons and Xiaoge, 2001) and, thus, keep invisible within the GPR index. The outcomes are largely comparable. Within the LP’s dynamic multipliers for the PRI, the rise within the oil value comes somewhat bit later, after 22 months, and lasts 10 months as within the baseline outcomes. The VAR’s dynamic multipliers for the PRI gives the same dynamics. In addition to, the outcomes are very comparable for the GPR index.

1989 Tiananmen Sq. occasions

Now, we begin the pattern for January 1985 the place the current GPR index is on the market. We’ll give attention to the 1989 Tiananmen Sq. occasions that happened between 15 April and 4 June 1989. We can not observe the identical discrepancy between the bilateral GPR and the PRI for the connection between US and China, that we observe for the US bombing of the Chinese language embassy in Belgrade. The rationale behind these outcomes is easy. Certainly, the worldwide media protection of the Tiananmen Sq. occasions is in keeping with the perceived deterioration in China of the relation with the US.

The outcomes of the dynamic multipliers are qualitatively comparable. Because the estimation interval is longer, we will be aware some variations within the LP’s and VAR’s dynamic multipliers for the true value of oil for the PRI. The rise within the oil value is obtained after 28 months and is shorter than within the baseline. This final result’s fascinating, as earlier than the Nineties, the Chinese language economic system has not a big affect on the world economic system. In addition to, the outcomes for the GPR are similar to the baseline outcomes. After the shock, the rise in the true value of oil comes somewhat bit later (10 months after the shock versus 8 months within the baseline) and lasts longer (22 months in opposition to 18 months within the baseline).

Contemplating the COVID pandemic

Now, we are going to take into account the impact of the COVID pandemic by increasing our pattern to January 2022. We cease our pattern in January 2022, earlier than the beginning of the warfare in Ukraine. As underlined by Baumeister (2023), the pandemic and the Russian invasion of Ukraine could have long-lasting results on the worldwide vitality panorama. After all, the outcomes of this peculiar sub-sample evaluation needs to be taken with a grain of salt, because the COVID outbreak constitutes an enormous, and short-lived, structural break in lots of macroeconomic time-series. Nevertheless, it may very well be fascinating to research how the mannequin behaves once we embrace the COVID interval.

The PRI index between the US and China has not identified any main shock throughout the COVID. The relation was in rival state and remained steady. Quite the opposite, the GPR index has identified a number of shocks. This hole is defined by the extra common nature of the GPR index. As talked about earlier than, the GPR index captures the point out of the geopolitical threat relative to China, however isn’t centered on the bilateral relation between China and the US. The results on the oil value dynamics are qualitatively comparable.

The outcomes are similar to these in with the pattern that begins from January 1985 and stops in December 2019. The rise within the oil value is obtained after 28 months and is shorter than within the baseline. In addition to, the outcomes are in keeping with baseline. The rise in the true value of oil lasts even longer (22 months in opposition to 18 months within the baseline).

Conclusion

The outcomes converge towards a constructive causal affect of bilateral political relationships between China and the US, and geopolitical dangers for China over the short-to-medium run. Nevertheless, these two quantitative measures usually are not absolutely substitutable, as they measure totally different dimensions of geopolitical relationships. As famous by Bondarenko et al. (2023), the notion of geopolitical threat in every nation could matter to measure the affect of those dangers on the economic system. This final level has been illustrated with the US bombing of the Chinese language embassy in Belgrade. In addition to, the PRI is extra centered on the bilateral relation between China and the US and displays expectations on the world demand for oil. The GPR index for China is extra common and displays fears of provide disruptions.

Bibliography

Abdel-Latif, H. and El-Gamal, M. (2020), ‘Monetary liquidity, geopolitics, and oil costs’, Power Economics 87, 104482.

Baumeister, C. (2023), Pandemic, warfare, inflation: Oil markets at a crossroads?, Working Paper 31496, Nationwide Bureau of Financial Analysis. URL: https://www.nber.org/papers/w31496

Baumeister, C. and Hamilton, J. D. (2019), ‘Structural interpretation of vector autoregressions with incomplete identification: Revisiting the position of oil provide and demand shocks’, American Financial Evaluation 109(5), 1873– 1910.

Bondarenko, Y., Rottner, M. and Schüler, Y. (2023), Geopolitical threat perceptions, Technical report, CEPR Dialogue Papers. URL: https://cepr.org/publications/dp18123

Cai, Y., Mignon, V. and Saadaoui, J. (2022), ‘Not all political relation shocks are alike: Assessing the impacts of US–China tensions on the oil market’, Power Economics 114, 106199.

Caldara, D., Conlisk, S., Iacoviello, M. and Penn, M. (2023), ‘Do geopolitical dangers increase or decrease inflation?’, Technical report.

Caldara, D. and Iacoviello, M. (2018), Measuring geopolitical threat, Technical report, Board of Governors of the Federal Reserve System. URL: https://doi.org/10.17016/IFDP.2018.1222r1

Caldara, D. and Iacoviello, M. (2022), ‘Measuring geopolitical threat’, American Financial Evaluation 112(4), 1194–1225.

Chen, H., Liao, H., Tang, B.-J. and Wei, Y.-M. (2016), ‘Impacts of OPEC’s political threat on the worldwide crude oil costs: An empirical evaluation based mostly on the SVAR fashions’, Power Economics 57, 42–49.

Goldstein, J. S. (1992), ‘A conflict-cooperation scale for WEIS occasions knowledge’, Journal of Battle Decision 36(2), 369– 385.

Jordà, Ò. (2005), ‘Estimation and inference of impulse responses by native projections’, American Financial Evaluation 95(1), 161–182.

Lee, C.-C., Lee, C.-C. and Ning, S.-L. (2017), ‘Dynamic relationship of oil value shocks and nation dangers’, Power Economics 66, 571–581.

Miao, H., Ramchander, S., Wang, T. and Yang, D. (2017), ‘Influential elements in crude oil value forecasting’, Power Economics 68, 77–88.

Parsons, P. and Xiaoge, X. (2001), ‘Information framing of the Chinese language embassy bombing by the Individuals’s Each day and the New York Instances’, Asian Journal of Communication 11(1), 51–67.

Perifanis, T. and Dagoumas, A. (2019), ‘Residing in an period when market fundamentals decide crude oil value’, The Power Journal 40(SI), 317–335.

Ponniah, Ok. and Marinkovic, L. (2019), ‘The night time the US bombed a Chinese language embassy’, BBC Information. URL: https://www.bbc.com/information/world-europe-48134881

Qin, Y., Hong, Ok., Chen, J. and Zhang, Z. (2020), ‘Uneven results of geopolitical dangers on vitality returns and volatility underneath totally different market situations’, Power Economics 90, 104851.

Yan, X. (2010), ‘The instability of China–US relations’, The Chinese language Journal of Worldwide Politics 3(3), 263–292.

This publish written by Jamel Saadaoui.

[ad_2]

Source_link