[ad_1]

Reader Econned asks me for a critique of ecological monetarism. I don’t have one total evaluation, however I’ll say that I don’t perceive (1) how Cameron Harwick got here up with the conclusion that the case for ecological monetarism was confirmed by inflation outcomes, and relatedly (2) how the beneath graph was constructed, which I consider is the idea for that conclusion.

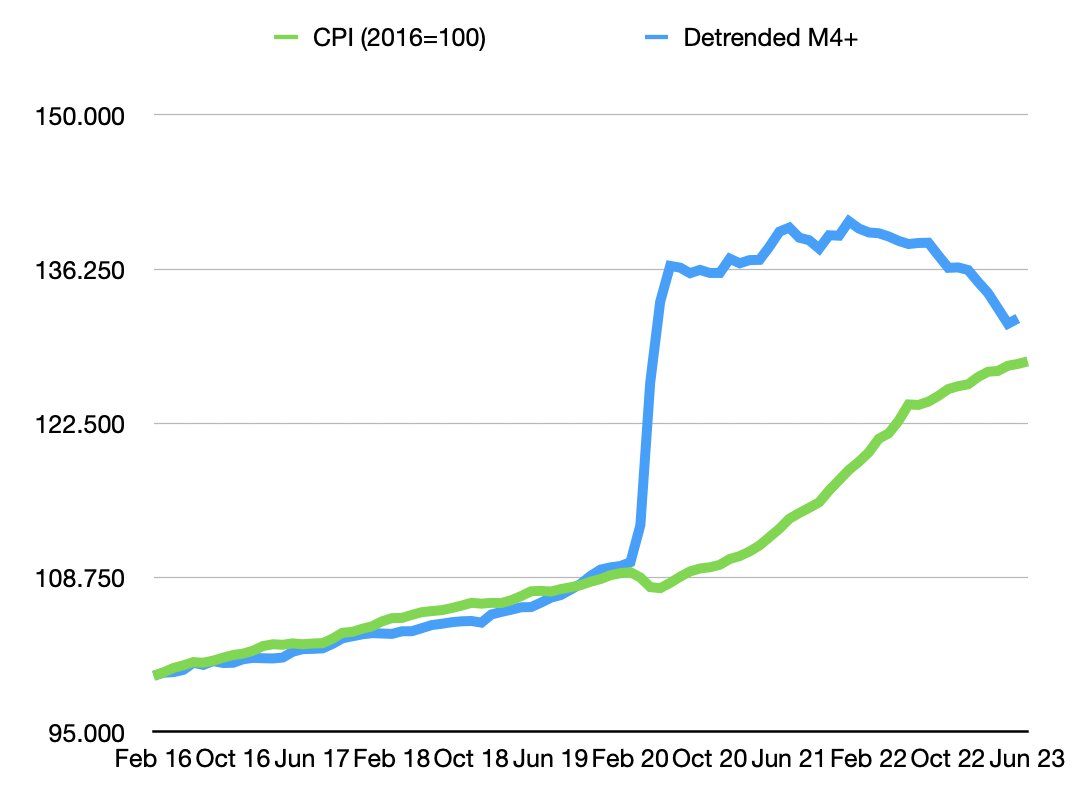

Right here is Harwick’s graph.

Supply: C. Harwick (2023).

Definitely, the graph appears to point the precise value stage and cash (detrended) match up fairly carefully by June 2023.

Sadly, the article doesn’t say how M4+ is detrended. It was clearly not a Hodrick-Prescott filter that was used (I attempted that).

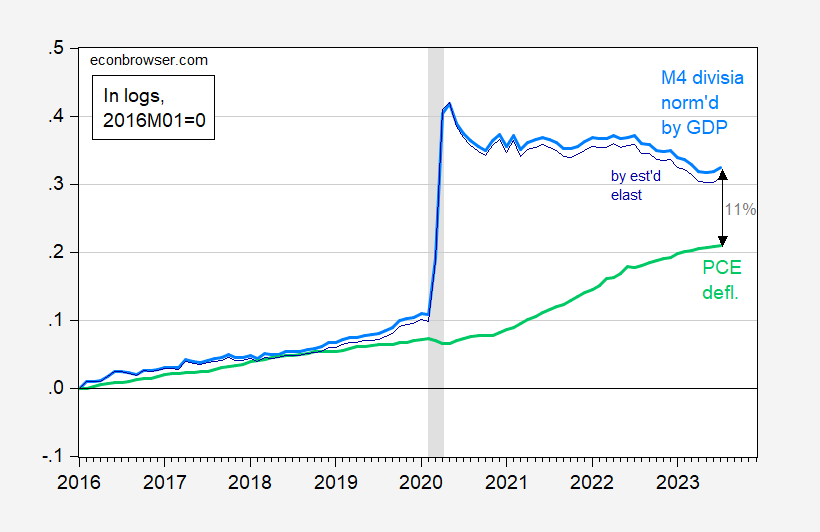

I detrended by dividing by GDP, which is in step with some variations of the Amount Principle. This yields the analogous image (in logs):

Determine 1: PCE value deflator (mild inexperienced), M4 divisia divided by actual GDP (mild blue), m4 divisia divided by GDP to the 1.1 energy (darkish blue), all in logs, 2016M01=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Cleveland Fed, SPGMI, CFS, NBER, and creator’s calculations.

[Observations for 2023M07 for PCE deflator is the Cleveland Fed nowcast as of 8/29; for GDP is forecasted using lagged GDP and current NFP.]

The hole between the value stage measured utilizing the PCE deflator and normalized divisia M4 is 11% as of July. One would possibly argue that detrending by GDP is inappropriate; perhaps it’s higher to make use of the earnings elasticity of actual cash demand, estimated from a cash demand equation. Utilizing Johansen over the 1967-2019 interval yields an elasticity of about 1.1. Utilizing this estimate results in a niche of 10% (and widening!).

As an apart, if we have been residing in a flex-price monetarist world, the value stage ought to’ve jumped on the similar time divisia cash elevated, by about 30%. Clearly, that didn’t occur.

Ultimately, with the intention to differentiate between fashions, one might have to match predictive energy (e.g., right here). I haven’t accomplished that comparability not too long ago, however I’ve estimated how an expectations and provide shock augmented Phillips curve does. If one thinks about how inflation has come down not too long ago in keeping with measured cost-push shocks (e.g., the NY Fed GSCPI), then one would possibly say the Phillips curve makes extra sense than the amount concept.

[ad_2]

Source_link