[ad_1]

I’ve puzzled about what a “smooth touchdown” entails, and whether or not we’re are headed towards one (see dialogue of diverging forecasts, in present difficulty of the Economist) That is regardless of findings that, primarily based on historic correlations, nearly any time period unfold primarily based regression will predict a recession by round mid-2024.

Booker and Wessel talk about the problem of sentimental landings, and cite this desk tailored from Blinder.

Supply: Boocker and Wessel (2023).

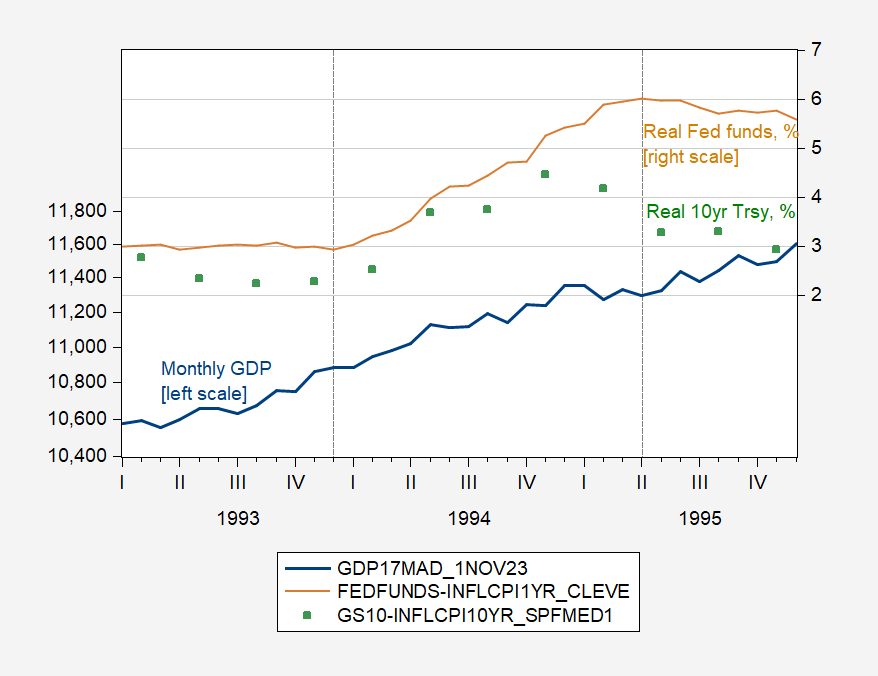

I’d solely been aware of the 1993-95 and 1999-2000 episodes. I believe it of curiosity to check the 1993-95 episode to the present, by way of actual charges and GDP. First, 1993-95:

Determine 1: Month-to-month GDP in bn.Ch.2017$ SAAR (blue, left log scale), Fed funds adjusted by Cleveland Fed 1 yr anticipated inflation, % (tan, proper scale), and ten yr Treasury yield adjusted by SPF 10 yr median anticipated inflation, % (blue, proper scale). Dashed traces at Boocker-Wessel-Blinder smooth land begin/finish. Supply: SPGMI, Federal Reserve Board and Treasury by way of FRED, Cleveland Fed, Philadelphia Fed, and creator’s calculations.

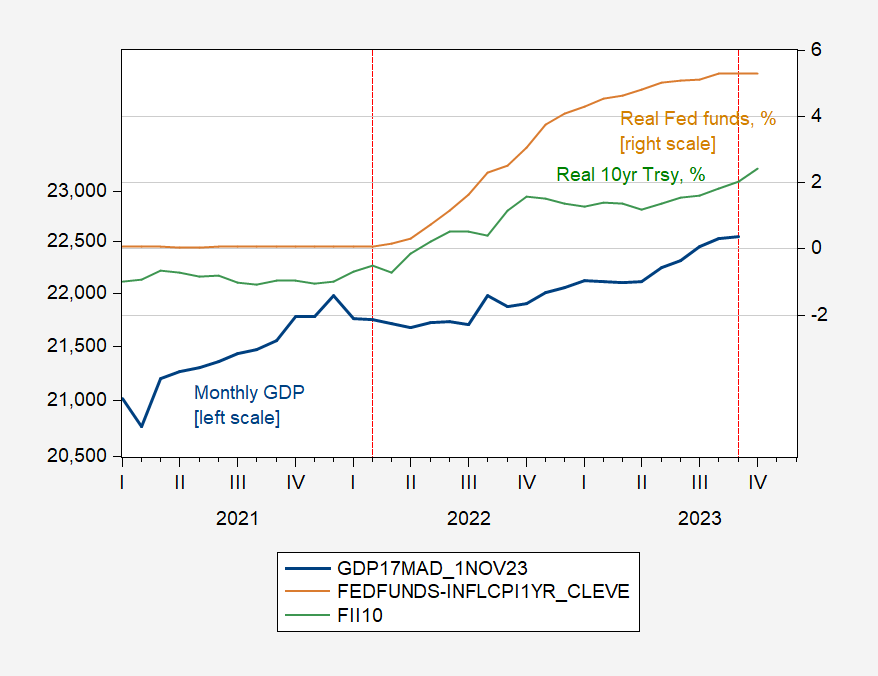

And right here’s the present episode of some type of touchdown, but to be decided…

Determine 2: Month-to-month GDP in bn.Ch.2017$ SAAR (blue, left log scale), Fed funds adjusted by Cleveland Fed 1 yr anticipated inflation, % (tan, proper scale), and ten yr TIPS, % (blue, proper scale). Dashed traces smooth land begin/finish as decided by creator. Supply: SPGMI, Federal Reserve Board and Treasury by way of FRED, Cleveland Fed, and creator’s calculations.

The latest episode has witnessed a bigger soar in actual Fed funds price (over 4.5% vs. 3%), an analogous enhance in the actual 10 yr Treasury, whereas output really decreased when the Fed funds rose (in 2022Q2) whereas it continued to rise in 1994. Additionally in distinction, by the tip of the smooth touchdown as outlined by Blinder, the ten yr actual price was declining, whereas within the present episode, that price continues to rise.

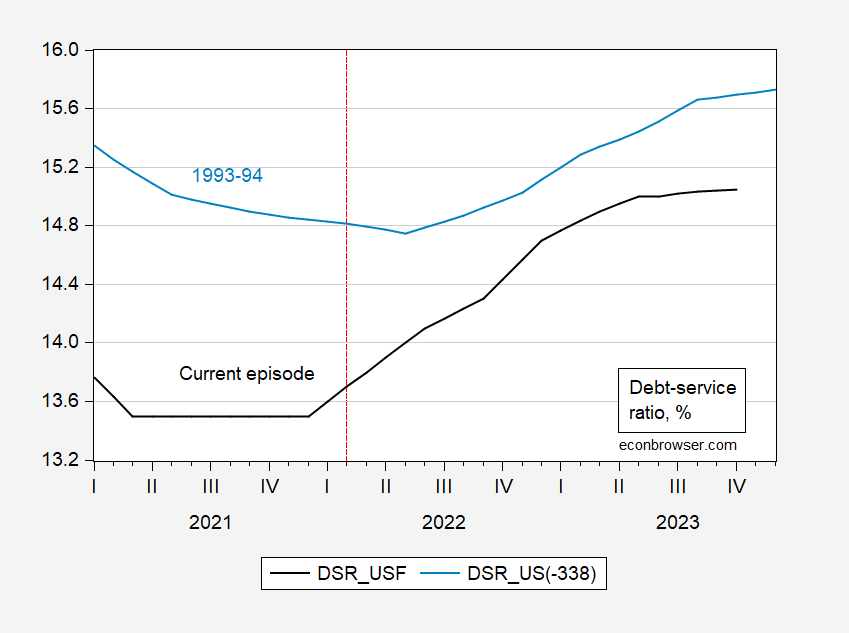

The debt service ratio has risen extra, as a consequence of the bigger rate of interest enhance.

Determine 3: Debt service ratio for personal nonfinancial sector now, in % (black), in 1993-95 in % (gentle blue). 2023M04-10 interval extrapolated utilizing 3 month rate of interest in first variations. Supply: BIS, and creator’s calculations.

In response to my guesstimates, the debt service ratio trajectory has flattened (precise information solely extends as much as 2023M03), however at a degree considerably increased than existed earlier than tightening started.

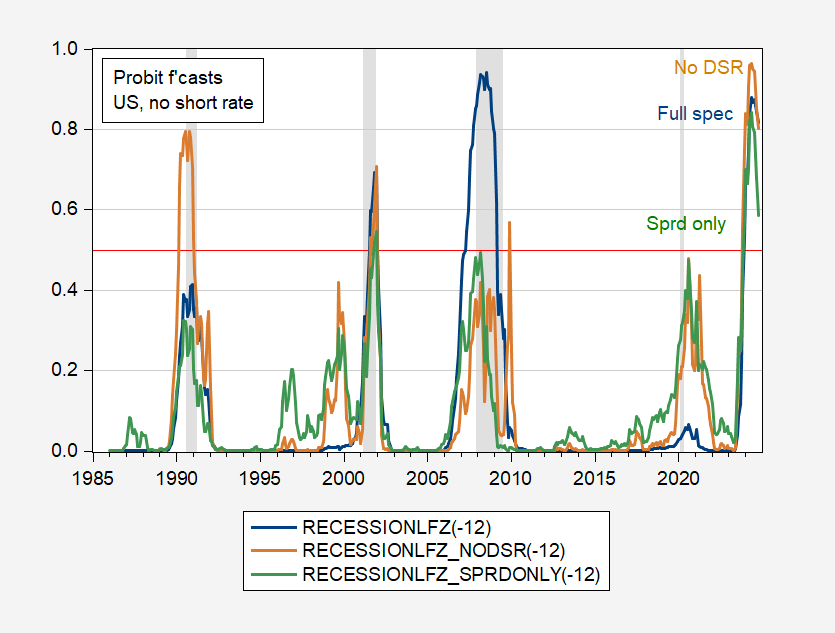

Because the smooth touchdown calls proceed, it’s helpful to recall that if historic correlations maintain, recession possibilities from spread-based probit fashions breach the 50% threshold round November-December of this yr, and peak round Might-June 2024.

Determine 4: Recession chance from probit mannequin with solely 10yr-3mo unfold (inexperienced), unfold, NFCI, overseas time period unfold (tan), and unfold, NFCI, debt-service ratio, overseas time period unfold (blue). NBER outlined peak-to-trough recession dates shaded grey. Supply: Creator’s calculations, NBER.

The vital caveat is that historic correlations maintain.

[ad_2]

Source_link