[ad_1]

The slowdown retains on being moved again — based on consensus — to This autumn. Imply forecast is for just one quarter of adverse development, however median has two (Q3, This autumn).

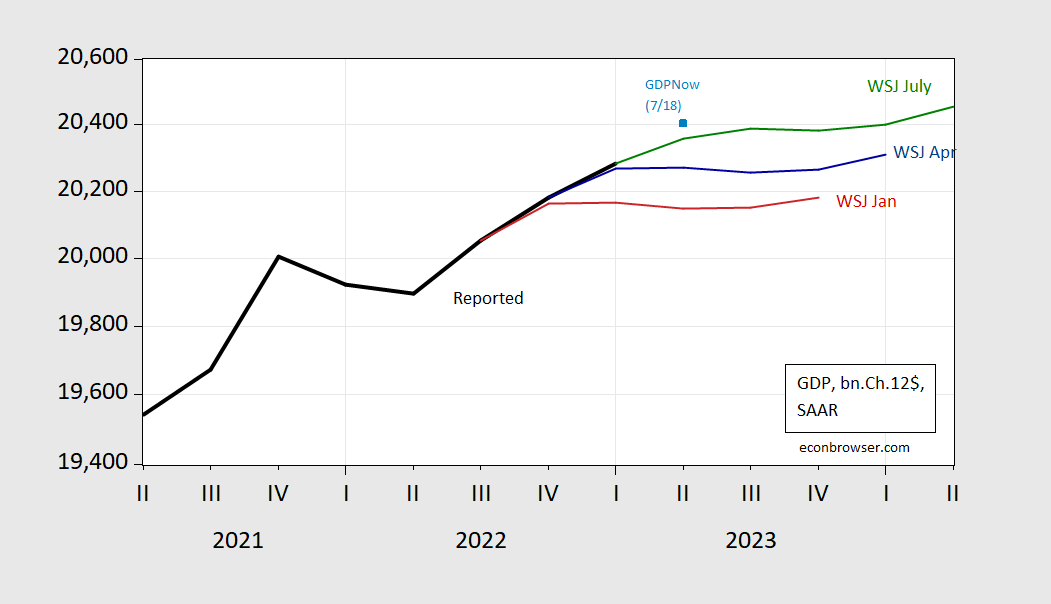

Determine 1: GDP (black), Imply forecast GDP from July WSJ survey (inexperienced), from April survey (blue), from January survey (purple), GDPNow nowcast of seven/18 (gentle blue sq.), all in bn.Ch.2012$ SAAR. Supply: BEA, WSJ surveys (numerous), and writer’s calculations.

Whereas the imply forecast trajectory retains on rising as precise GDP outcomes carry on stunning on the upside, forecasts are fairly dispersed, as proven in Determine 2.

Determine 2: GDP (black), Imply forecast GDP from July WSJ survey (inexperienced), median of Worth/Ameriprise Monetary (pink), 20% trimmed excessive of Feinup, Hamilton/Cal Lutheran Univ. (grey), trimmed low of Fratantoni/Mortgage Bankers Affiliation (grey), GDPNow nowcast of seven/18 (gentle blue sq.), all in bn.Ch.2012$ SAAR. Supply: BEA, WSJ surveys (numerous), and writer’s calculations.

The 20% trimmed excessive signifies 1.5% common annualized development over the following 5 quarters (imply/median foreast is 0.68%/0.66%). The trimmed low is 0.46% Word that the pattern excessive forecast (the irrepressible James F. Smith, now of EconForecaster) was 3%(!).

Recession possibilities from the survey, contrasted with time period unfold primarily based estimates — mentioned on this put up.

[ad_2]

Source_link