[ad_1]

Month-to-month GDP, as estimated by SPGMI (previously IHS Markit/Macroeconomic Advisers) drops 0.5% m/m (-6.3% annualized!)

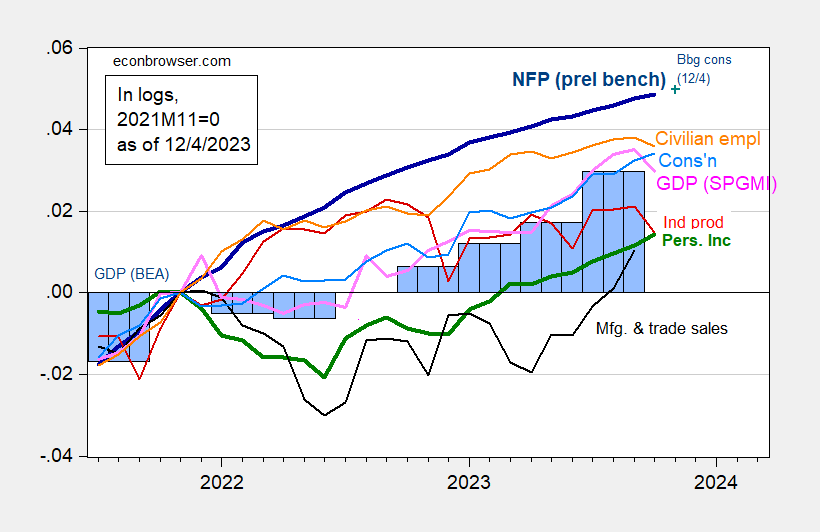

Determine 1: Nonfarm Payroll employment incorporating preliminary benchmark (daring darkish blue), implied stage utilizing Bloomberg consensus as of 12/4 (blue +), civilian employment (orange), industrial manufacturing (pink), private revenue excluding transfers in Ch.2017$ (daring inexperienced), manufacturing and commerce gross sales in Ch.2017$ (black), consumption in Ch.2017$ (mild blue), and month-to-month GDP in Ch.2017$ (pink), GDP, 2nd launch (blue bars), all log normalized to 2021M11=0. Supply: BLS by way of FRED, BLS preliminary benchmark, Federal Reserve, BEA 2023Q3 2nd launch incorporating complete revisions, S&P World/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (12/1/2023 launch), and creator’s calculations.

Civilian employment, industrial manufacturing and month-to-month GDP declined in October, whereas nonfarm payroll employment and private revenue ex-current transfers (each central NBER BCDC variables) continued to rise — as did consumption.

Whereas month-to-month GDP declined -0.5% m/m, remaining gross sales elevated 0.1% m/m. To the extent that this sequence extra carefully displays combination demand, the scenario seems extra constructive. SPGMI does, nevertheless, forecast a reasonably lackluster 0.9% q/q SAAR progress for This autumn.

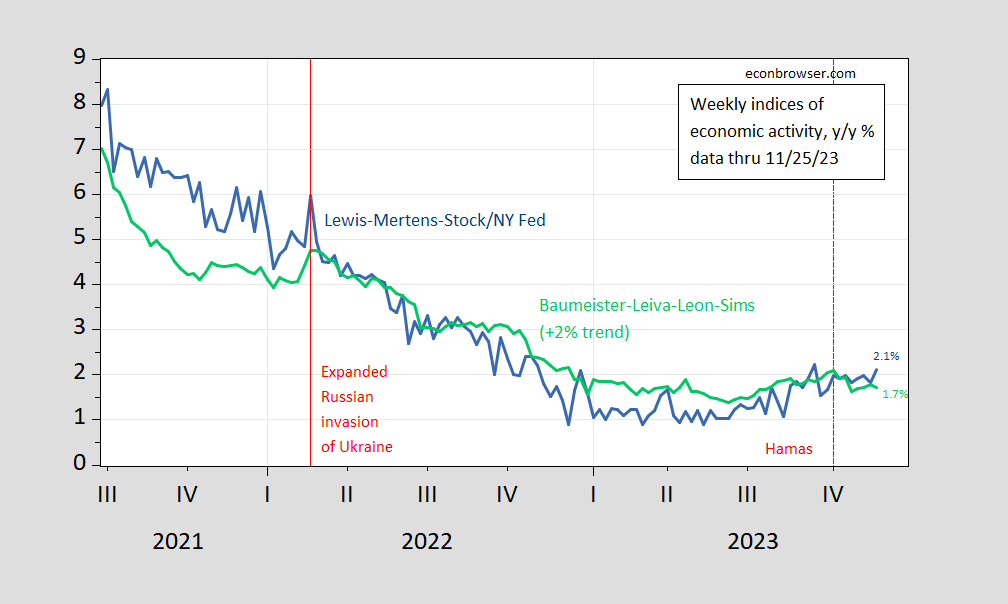

These are backwards wanting variables which can be utilized by the NBER’s BCDC to find out enterprise cycle turning factors. Larger frequency (weekly) information by means of releases obtainable by 11/25 point out progress roughly at pattern.

Determine 2: Lewis-Mertens-Inventory Weekly Financial Index (blue), and Baumeister-Leiva-Leon-Sims Weekly Financial Situations Index for US plus 2% pattern (inexperienced), all y/y progress price in %. Supply: NY Fed by way of FRED, WECI, accessed 12/4, and creator’s calculations.

[ad_2]

Source_link