[ad_1]

“I want the US Greenback to be a retailer of worth between the time I make it till I spend it, make investments it, pay my taxes with it, or give it away. It does that splendidly.” 1

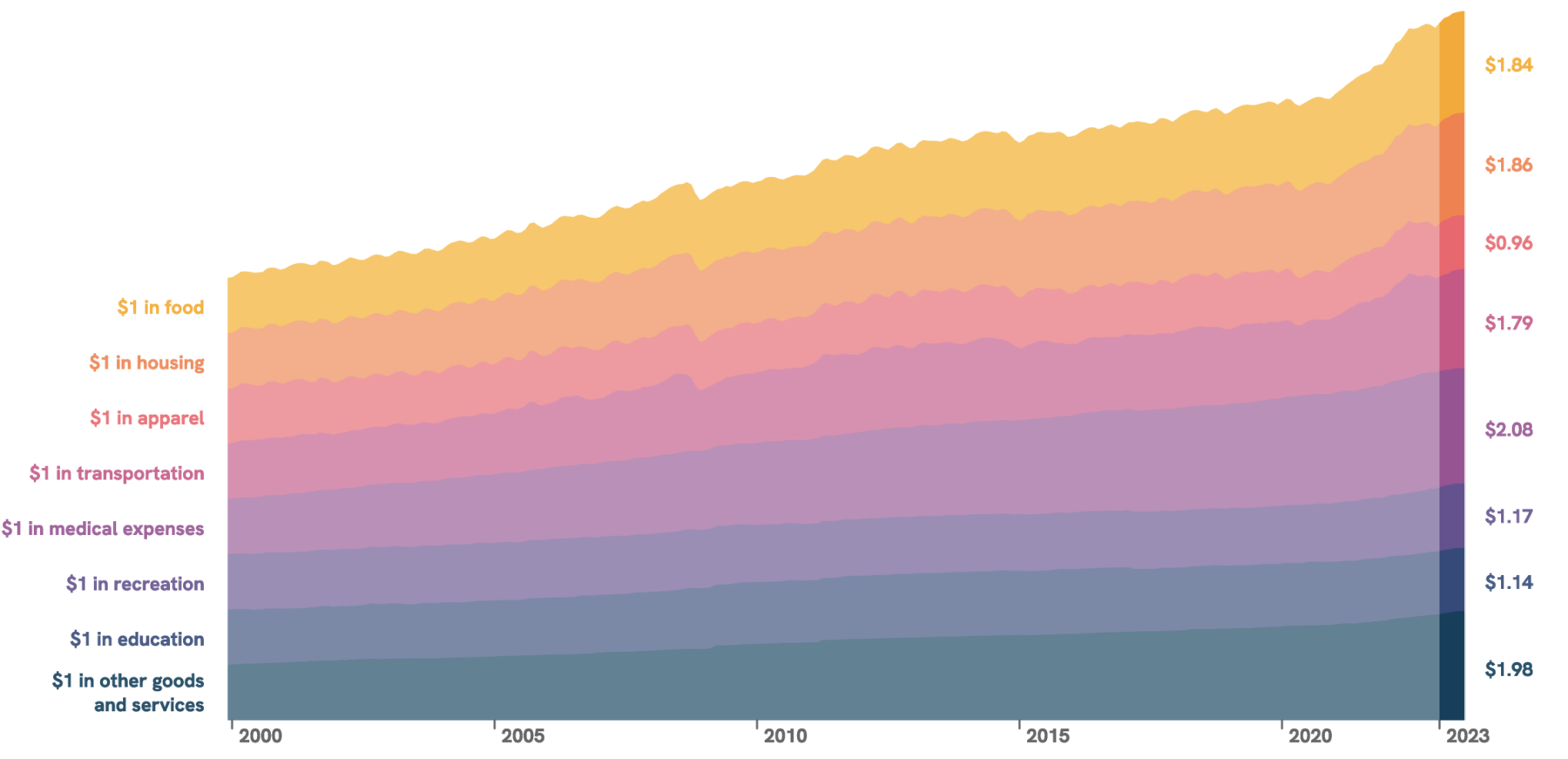

At the moment, we’re going to have a look at a perennial (un)favourite #chartfail. To be extra exact, I wish to focus on the kind of chart that displays a elementary misunderstanding of the character of cash, foreign money, spending, investing, and taxes. I’ve talked about this within the previous, however I occurred throughout the chart above, and it serves as a reminder to revisit this subject in better element.

You receives a commission in {dollars}. That compensation is in a foreign money that could be a extensively accepted medium of trade.

For instance, I work 40-60 hours per week; I receives a commission for my time and efforts. That comp will get deposited instantly into my checking account; that cash is obtainable for buying requirements (meals, housing, clothes, drugs, transportation, and many others.), discretionary spending (leisure, journey, and many others.), and for paying my taxes.

However that’s not all: I even have the chance to make investments these {dollars}: I should buy a broad market index, patiently ready for it to understand; I should buy bonds and benefit from the earnings they yield; I might buy actual property, which both offers me a spot to dwell or lease out for earnings; I might additionally use that cash to begin or construct a enterprise.

In every of these 4 classes, the {dollars} I make investments will generate a return over time. And over the previous few centuries, these returns have enormously exceeded inflation. And that’s the important thing misunderstanding of charts just like the one above: It ignores the time worth of cash.

Whether or not it’s just a few many years or a century, the mathematics works the identical.

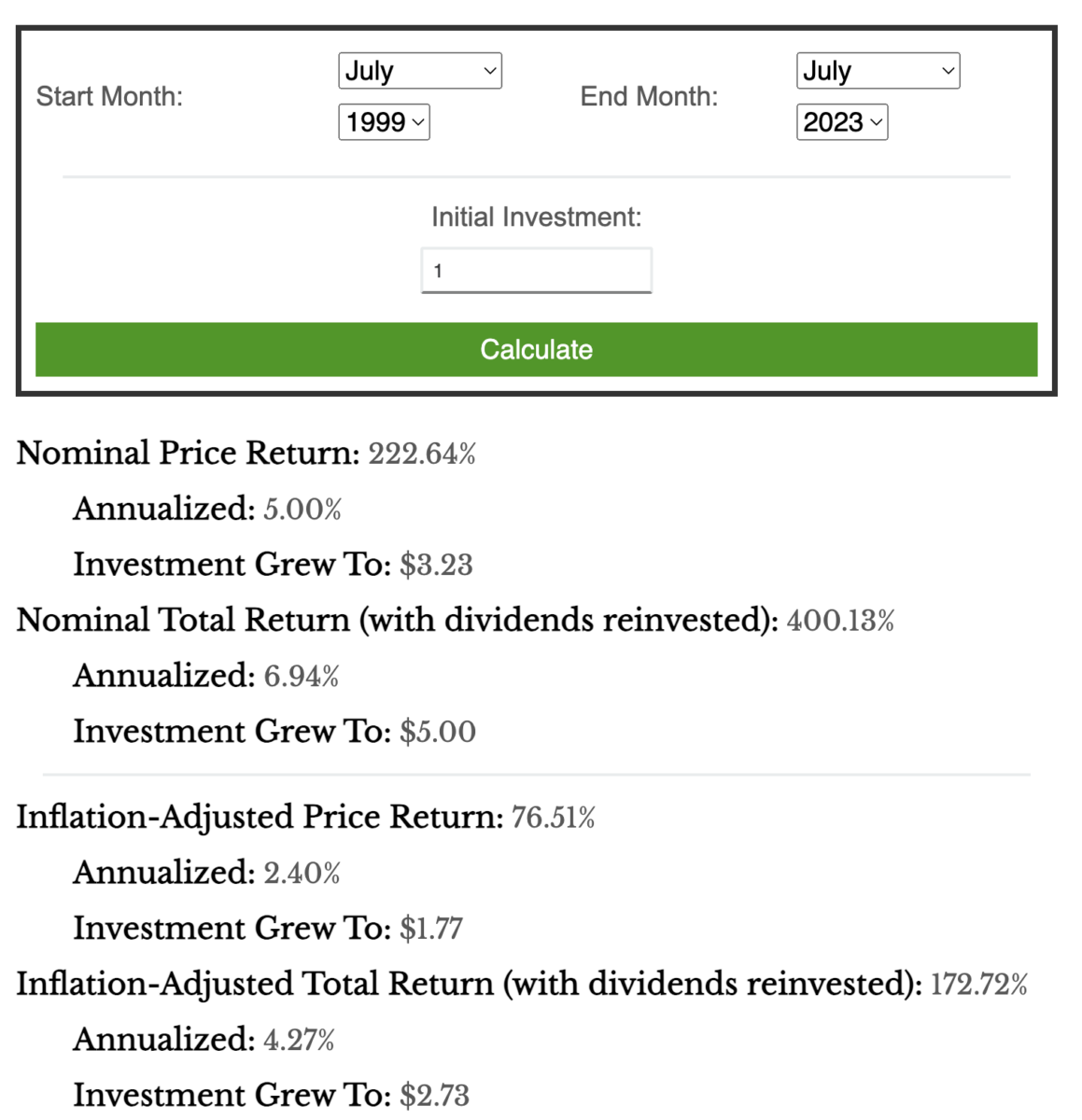

Again to our colourful chart at prime. Certain, it now takes $1.84 to purchase that greenback of 1999 meals. However had you set that right into a easy funding just like the S&P500 as a substitute of holding the {dollars}, it will have grown at an annual charge of 6.94% per yr and be price about $5 {dollars}.2 You could possibly purchase these groceries and nonetheless have $3.16 left over.

Again to our colourful chart at prime. Certain, it now takes $1.84 to purchase that greenback of 1999 meals. However had you set that right into a easy funding just like the S&P500 as a substitute of holding the {dollars}, it will have grown at an annual charge of 6.94% per yr and be price about $5 {dollars}.2 You could possibly purchase these groceries and nonetheless have $3.16 left over.

Hey, what a really totally different consequence than suggesting a lack of buying energy — for those who perceive cash and math, you might have really gained buying energy.

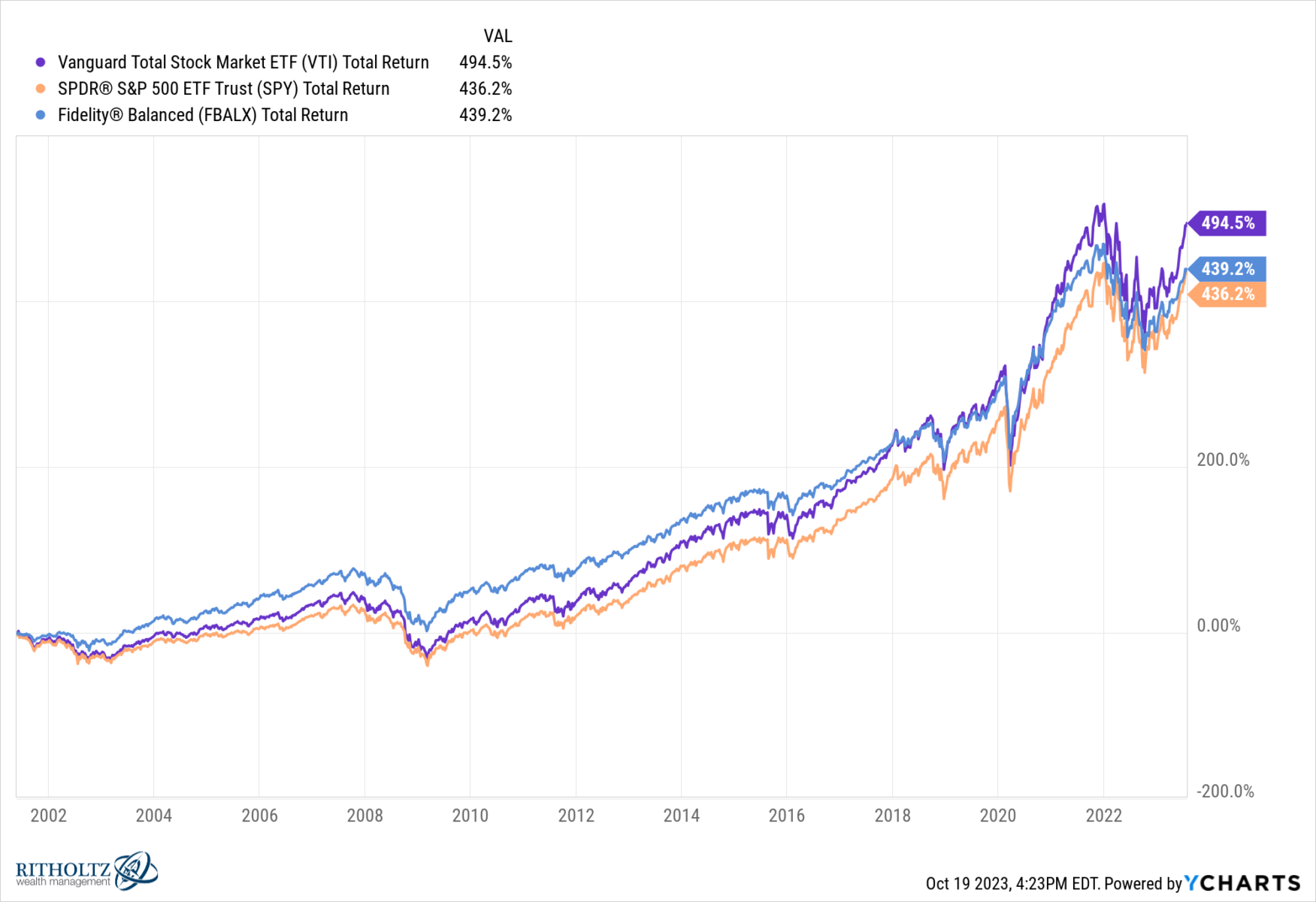

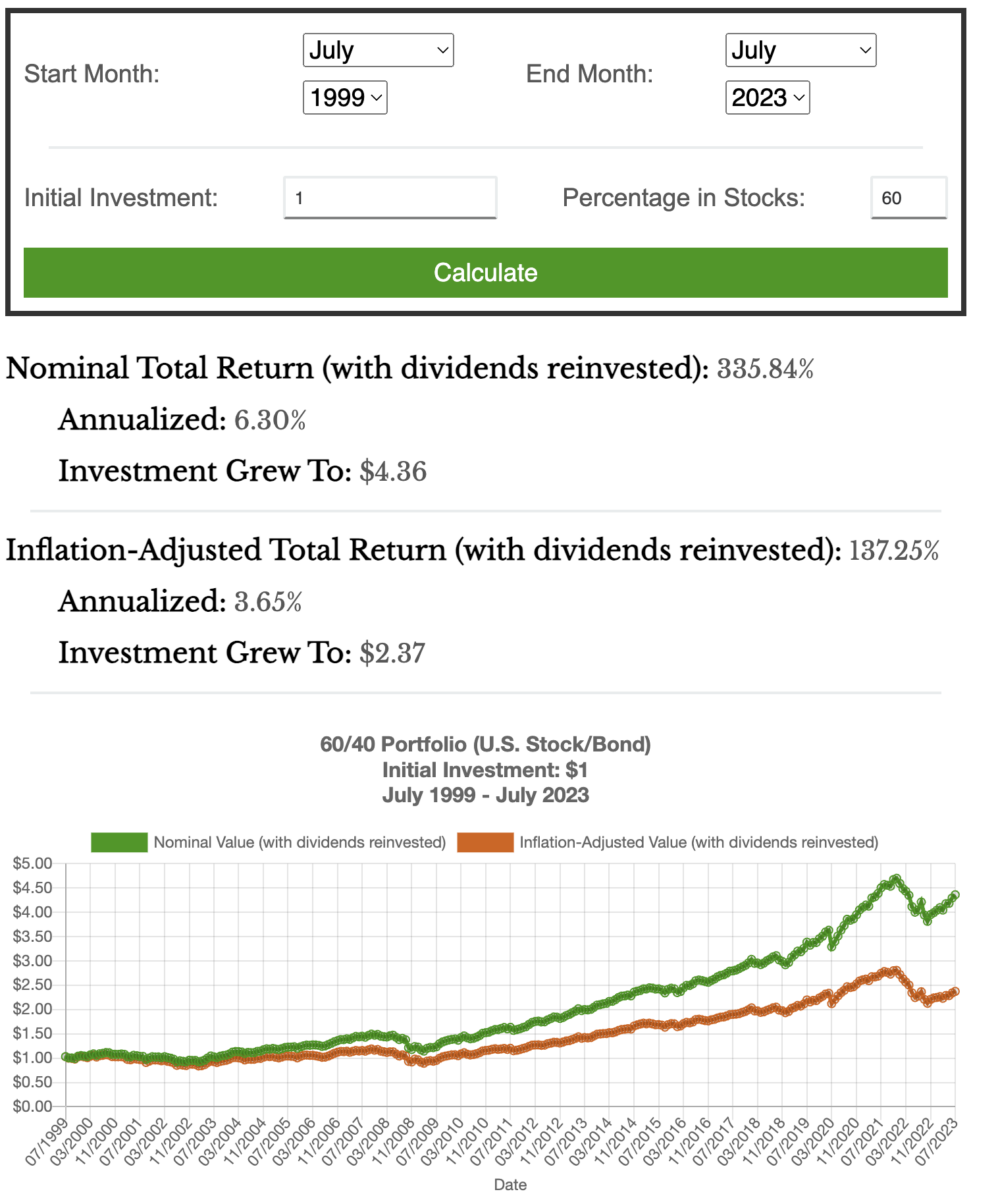

As a substitute of cherry-picking the S&P 500, what a few easy 60/40 portfolio (e.g., Constancy Balanced Fund, FBALX)? You’ll have finished barely worse, gaining about 6.7% per yr.3 And the Vanguard Complete Market (VTI) would have finished barely higher, garnering about 7.8% yearly over the identical interval.4

I at all times dislike these one-sided arguments – Come see how a lot the greenback has depreciated over a century! At greatest, it’s denominator blindness; at worst, it’s purposefully deceptive, ignorant, or full-blown Russian propaganda. All I do know is these are crap charts that reveal little aside from their creator’s elementary misunderstanding of finance.

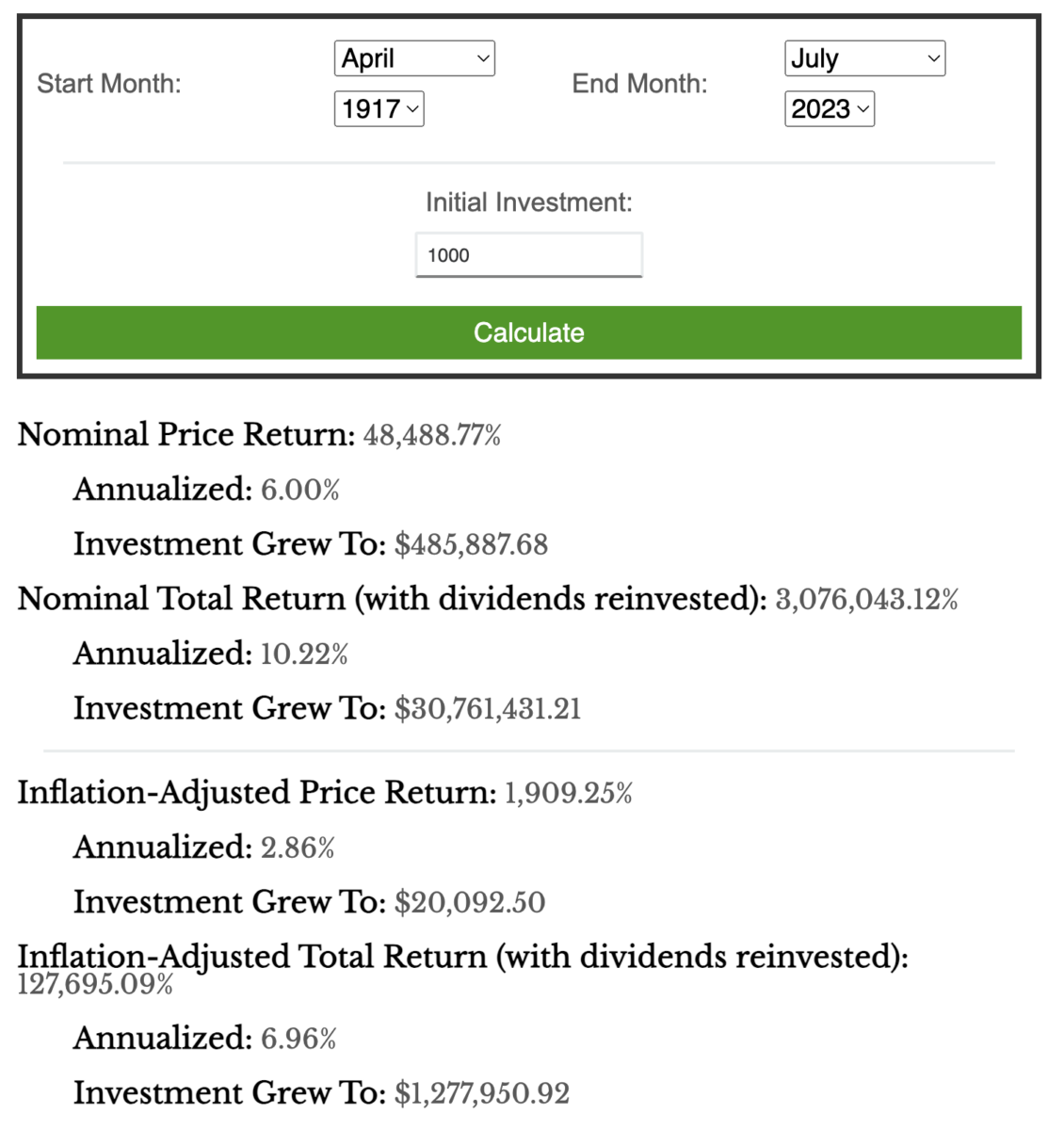

Let’s think about two folks, every with $1,000 {dollars}, on the point of go off to World Battle I in April 1917. One decides to bury the money in mason jars within the yard, whereas the opposite units up an account invested out there (held in a belief in case they don’t return). Their descendants every take possession of those in July 2023. If it was your great-grandpappy who buried the money, sorry, it’s now price 96% lower than April 1917. But when it was your ancestor who put that $1,000 into equities over that very same interval, nicely congratulations. Since then, markets have returned about 10.22% a yr, and that small fortune grew to an unlimited one,5 now price over $30 million.6

Forex just like the U.S. Greenback is a medium of trade, not a retailer of worth. As such, they’re by no means purported to be left hanging round for years or many years; burying them for hundreds of years is simply laughable.

{Dollars} are for spending and investing; they’re a medium of trade, not a retailer of worth, and they don’t seem to be simply counting…

Supply:

How Far Does $1 From 1999 Go At the moment?

by Shri Khalpada

PerThirtySix, August 14, 2023

__________

1. My Tweet from 10:33 AM · Oct 12, 2021

2. $1 within the S&P500 with dividends reinvested grew 6.94% annualized; over that 24-year interval it will have grown to $5.00; knowledge returns from Nick Maggiulli’s S&P 500 Historic Return Calculator [With Dividends]

3. $1 within the 60/40 portfolio with dividends reinvested grew at 6.30% annualized; over that 24-year interval it will have grown to $4.36 ; knowledge returns from Nick Maggiulli’s U.S. Inventory/Bond Historic Return Calculator.

4. $1 within the Vanguard Complete Inventory Market ETF (VTI) with dividends reinvested grew 7.87% annualized; over that 24-year interval, it will have grown to about $5.67.

5. $1,000 within the S&P500 with dividends reinvested would return 10.22% annualized, and from April 1917 to July 2023 could be price $30,761,431.21; knowledge returns from Nick Maggiulli’s S&P 500 Historic Return Calculator [With Dividends]

6. Returns over this lengthy a interval are exponential, and subsequently not very intuitive.

A enjoyable manner to consider that is through the rule of 72. At 10.2%, annual returns, your $1,000 will double each ~7 years. Ranging from 1917, meaning the cash has doubled 15 instances:

| Yr | Greenback Quantity |

| 1917 | $1,000 |

| 1924 | $2,000 |

| 1931 | $4,000 |

| 1938 | $8,000 |

| 1945 | $16,000 |

| 1952 | $32,000 |

| 1959 | $64,000 |

| 1966 | $128,000 |

| 1973 | $256,000 |

| 1980 | $512,000 |

| 1987 | $1,024,000 |

| 1994 | $2,048,000 |

| 2001 | $4,096,000 |

| 2008 | $8,192,000 |

| 2015 | $16,384,000 |

| 2022 | $32,768,000 |

Fairly unbelievable, huh?

Matching the above 1999 inflation chart:

S&P500 Returns, July 1999 to July 2023

60/40 Returns, July 1999 to July 2023

[ad_2]

Source_link