[ad_1]

In a approach, sure — that’s when it comes to ranges. When it comes to tempo of change, no.

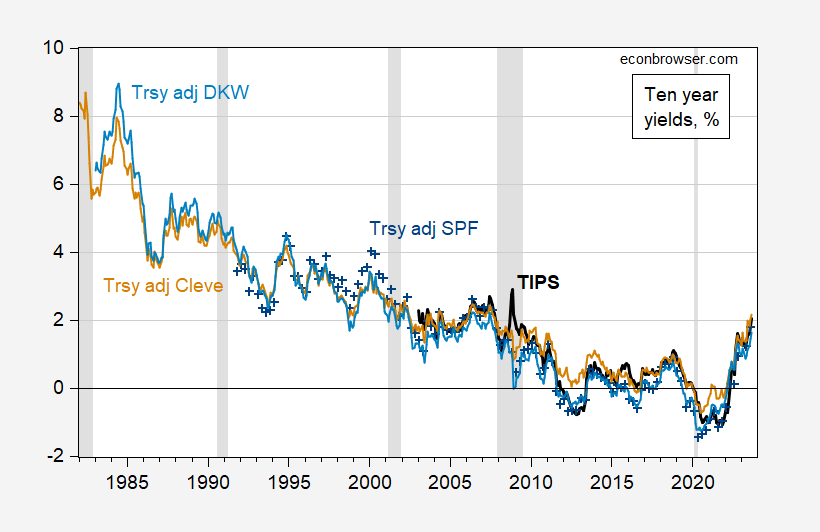

Determine 1: TIPS 10 yr (daring black), Treasury 10 yr minus Survey of Skilled Forecasters median 10 yr anticipated inflation (blue +), minus Cleveland Fed anticipated inflation (tan), minus KWW anticipated inflation (mild blue), all in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: Treasury through FRED, Philadelphia Fed, Cleveland Fed, KWW from Fed Board, NBER, and creator’s calculations.

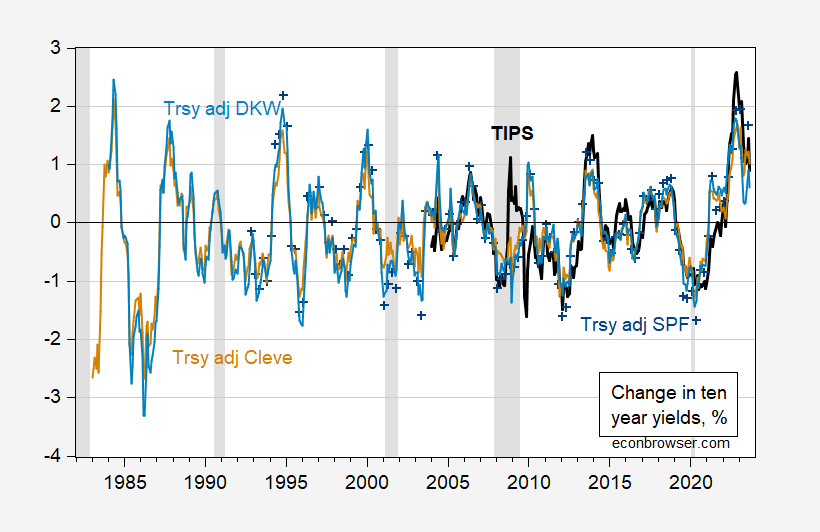

Nonetheless, wanting on the year-on-year change, the run-up in actual charges is unprecedented was unprecedented, by 2022M11. For twenty-four month adjustments, is is presently unprecedented (over this pattern interval).

Determine 2: 12 month adjustments in TIPS 10 yr (daring black), Treasury 10 yr minus Survey of Skilled Forecasters median 10 yr anticipated inflation (blue +), minus Cleveland Fed anticipated inflation (tan), minus KWW anticipated inflation (mild blue), all in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: Treasury through FRED, Philadelphia Fed, Cleveland Fed, KWW from Fed Board, NBER, and creator’s calculations.

Whereas the 12 month change within the 10 yr yield has moderated to about 2.3-3% from a peak of 0.9-2.4%, the annualized 24 month change is at a excessive of 1.5% (TIPS).

[ad_2]

Source_link