[ad_1]

From a brand new paper, NBER WP No. 32084, on my own and Laurent Ferrara, out at this time.

Summary: In recent times, there was renewed curiosity within the moments of the yield curve (or alternatively, the time period unfold) as a predictor of future financial exercise, outlined as both recessions, or industrial manufacturing progress. On this paper, we re-examine the proof for this predictor for america, different high-income international locations, in addition to chosen rising market economies (Brazil, India, China, South Africa and South Korea), over the 1995-2023 interval. We study the sensitivity of the outcomes to the addition of economic variables that measure different dimensions of economic circumstances each domestically and internationally. Particularly, we account for monetary circumstances indexes (Arrigoni, et al., 2022), the debt service ratio (Borio, et al., 2020), and overseas time period spreads (Ahmed and Chinn, 2023). We discover that overseas time period spreads and the debt service ratio in lots of instances yield considerably higher predictive energy, when it comes to in-sample match utilizing proportion of variance defined. Total, the predictive energy of the yield curve, in addition to different monetary variables, varies throughout international locations, with notably little explanatory energy in rising market economies.

For america, we now have the next outcomes, the place we assume no recession has occurred by 2023M02: In a parsimonious regression with solely time period unfold or time period unfold with brief price, the coefficients have anticipated signal. A monetary circumstances index additionally enters with vital and anticipated signal when added to this specification. Nevertheless, addition of a debt-service ratio (DSR) and a overseas time period unfold eliminates the importance of the time period unfold and FCI.

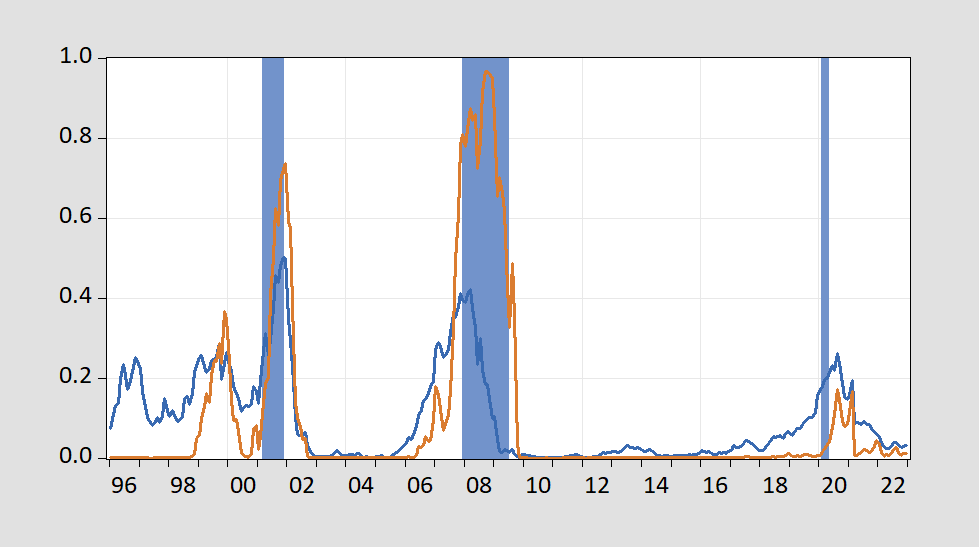

In-sample prediction utilizing the phrases unfold solely and all variables in Determine 1.

Determine 1: Estimated chance of recession from time period unfold solely (blue), time period unfold, brief price, FCI, DSR, overseas time period unfold (tan), and NBER peak-to-trough recession dates shaded blue. Supply: excerpt from Determine 2 of Chinn and Ferrara (2024).

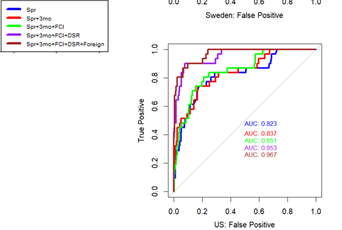

The AUROC for the varied fashions is proven in Determine 2.

Determine 2: AUROC for US specs. Supply: excerpt from Determine 3b of Chinn and Ferrara (2024).

Notice the AUROC is fairly excessive for the straightforward time period unfold specification. Nevertheless, addition of the debt-service ratio will increase prediction considerably. Curiously, the overseas time period unfold (as urged by Ahmed and Chinn (2023)) augments prediction even after addition of the DSR.

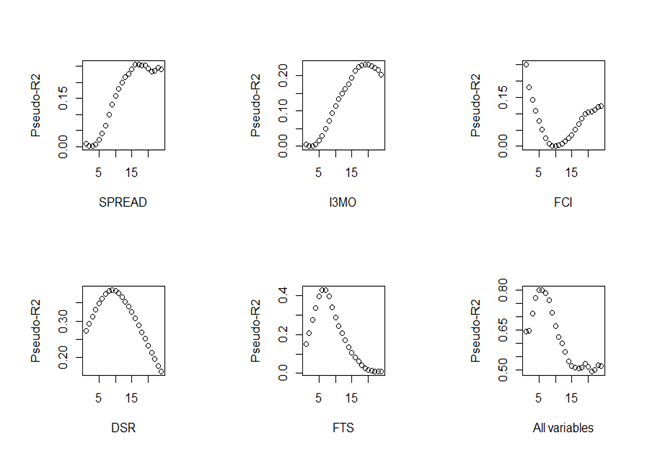

We assessed the predictive energy of the person variables on the completely different horizons.

Determine 3: Psuedo-R2s for US. Supply: Determine 4 from Chinn and Ferrara (2024).

The unfold and brief price proof peak prediction at a few yr and a half. In distinction, the overseas time period unfold has peak function at about 6 months. The DSR has most prediction at a few yr. All 5 variables, peak prediction at about 6 months, with pseudo-R2 at 0.8 (in comparison with 0.6 at 12 month horizon).

Ungated model of Chinn and Ferrara (2024).

[ad_2]

Source_link