[ad_1]

First time instructing undergrad macro (elective, after intermediate macro) in three years, so I believed time to revise the syllabus (Econ 442) to account for brand spanking new points (examine in opposition to Fall 2001).

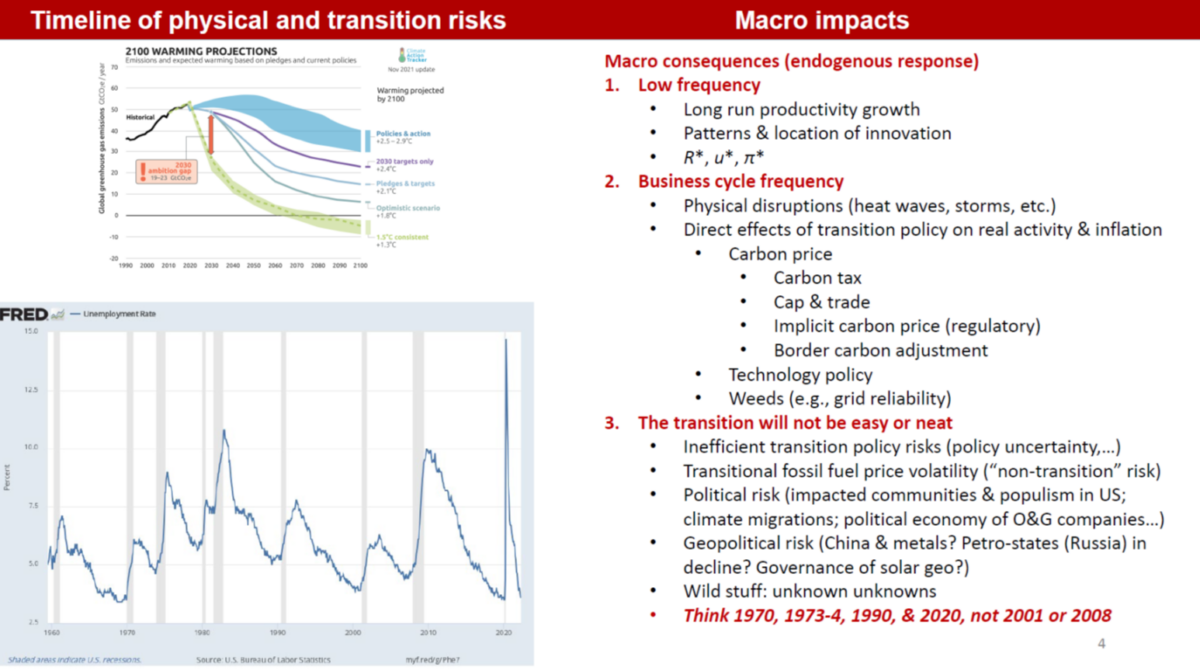

First, local weather change and macro implications.

Supply: Inventory (2022).

Will probably be specializing in local weather shocks complicating macro stabilization (take into account hurricanes, droughts, warmth waves, catastrophe insurance coverage crises), penalties of reliance on fossil fuels, implications of carbon taxes and cap & commerce.

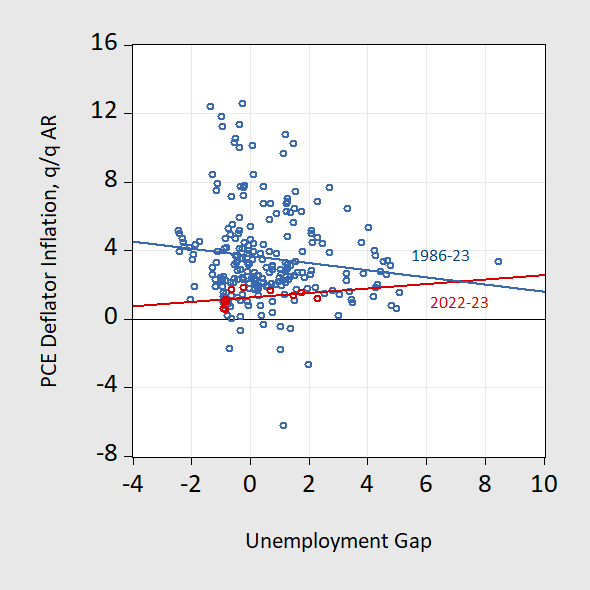

Is the Phillips Curve nonetheless related?

Determine 1: PCE deflator q/q Annualized inflation in opposition to unemployment hole, lagged one quarter, 1986-2023Q3. Bivariate regression line for 1986-2023 (blue), for 2021-2023 (crimson). Unemployment hole calculated as unemployment fee minus noncyclical unemployment fee from CBO. Supply: BEA, BLS, CBO through FRED, and writer’s calculations.

The fast runup and decline is taken by some as an indictment of the standard Phillips curve strategy. Determine 1 is suggestive. Nonetheless, even a fundamental textbook model of the Phillips curve incorporates greater than 2 variables…

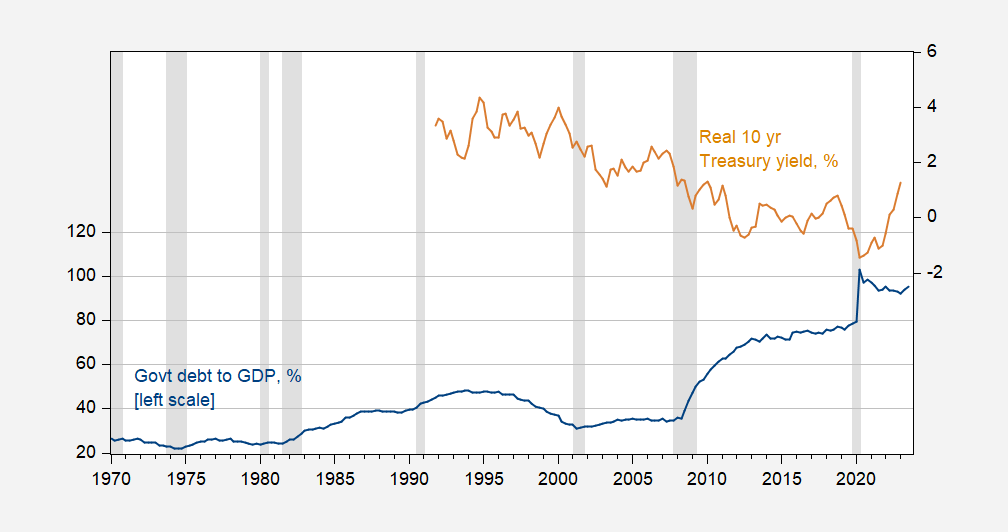

Is it authorities debt: why have actual yields risen?

Determine 2: Authorities debt held by public divided by GDP, % (blue, left scale), and actual 10 12 months Treasury yield, % (tan, proper scale). Actual yield is nominal 10 12 months subtracting SPF anticipated 10 12 months inflation fee. NBER outlined peak-to-trough recession dates shaded grey. Supply: Treasury, BEA, through FRED, Philadelphia Fed, NBER, and writer’s calculations.

The change from declining debt-to-GDP to rising in 2001, accompanied by fall actual yields posed a problem to standard knowledge. Did the 2020 soar in debt-to-GDP end in a long-standing break in that affiliation.

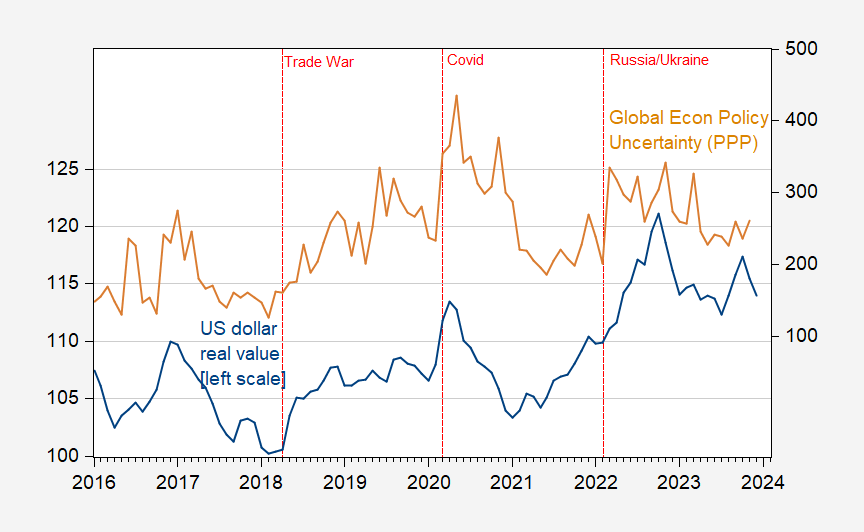

Will the greenback stay a safe-haven foreign money (and what does it suggest for rates of interest)?

Determine 3: US greenback (broad) actual worth (blue, left scale), and World Financial Coverage Uncertainty, PPP weighted (tan, proper scale). Actual trade fee spliced at 2006M01 – items weights pre-2006, items and providers weights thereafter. Supply: Federal Reserve Board, policyuncertainty.com, and writer’s calculations.

In instances of uncertainty, the greenback rises in worth. That is even true when when shock emanates from the US (suppose Covid and bleach; and in September 2008).

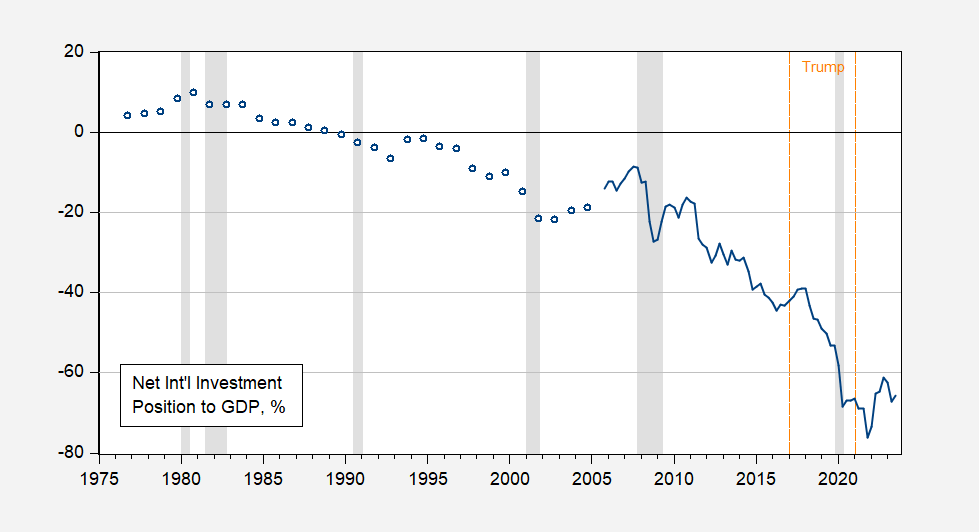

And what does reserve foreign money standing (associated however totally different from being a protected have foreign money) suggest for continuation of this pattern within the US Internet Worldwide Funding Place?

Determine 4: Internet worldwide funding of the USA (ex-derivatives) as a share of US GDP, %. NBER outlined peak-to-trough recession date shaded grey. Supply: BEA, NBER and writer’s calculations.

Curiously, the US turned more and more a web debtor (by about 30 ppts of GDP) over the Trump administration. Profitable!

The textbook for the category is Olivier Blanchard’s Macroeconomics. I do know some folks will ask “what the he** do you train your college students, Menzie?” (That query is requested by the similar one that argued {that a} recession occurred in 2022H1). Now you realize.

By the way in which, for the primary time in three years, I don’t get to show MSc. macro. However right here’s the syllabus for final 12 months’s Econ 702 (textbook by Garin, Lester, and Sims).

[ad_2]

Source_link