[ad_1]

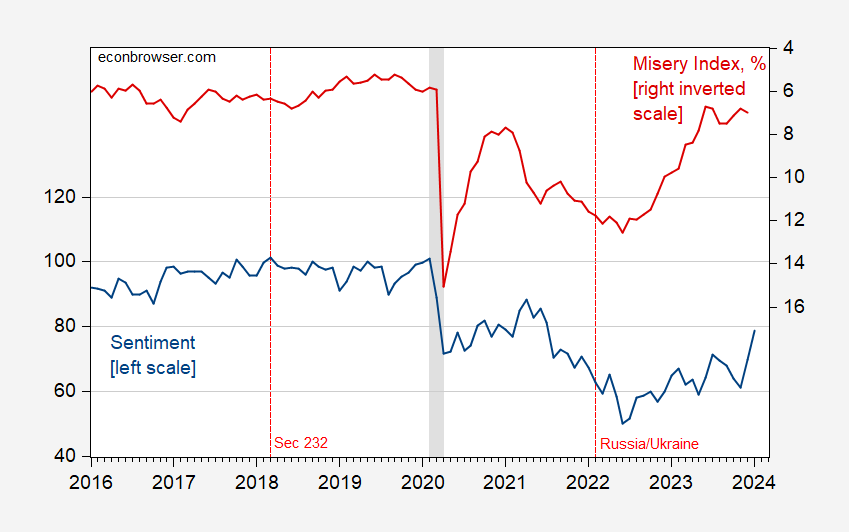

One of many mysteries of current occasions has been the divergence between circumstances (say, as measured by the Distress Index) and measured shopper sentiment. Determine 1 exhibits the U.Michigan sentiment index (FRED variable UMCSENT) vs. the sum of inflation and unemployment charges over the 2016-24M01 interval. The leap in UMCSENT of 9 was about 2 customary deviations (for the 2016-23 interval), on prime of the practically two deviation leap in December, and goes some option to redressing the hole.

Determine 1: College of Michigan Client Sentiment ) (FRED sequence UMCSENT) (blue, left scale), and Distress Index, % (crimson, inverted proper scale). NBER outlined peak-to-trough recession dates shaded grey. Supply: College of Michigan through FRED, BLS, NBER, and creator’s calculations.

The Distress Index is inverted so increased values point out decrease distress. The Distress Index begins rising round mid-2022, relative to measured financial sentiment. Utilizing a regular OLS regression of sentiment on distress over this era, residuals are considerably completely different from zero beginning round mid-2022. One other option to put that is that as of December 2023, the anticipated studying for UMCSENT is 88, whereas the precise was about 70.

One fascinating stylized reality is that the correlation between inflation expectations from U.Michigan and UMCSENT is excessive, rising from zero 2016-2019 to 0.70 for 2020-2024M01. This means an outsize affect of inflation. One other manner to have a look at that is to check the standardized betas pre- and post-pandemic. The betas for unemployment charge and inflation are about equal pre-pandemic. From 2020M01 onward, the inflation beta coefficient is about 4 occasions that of the unemployment beta coefficient.

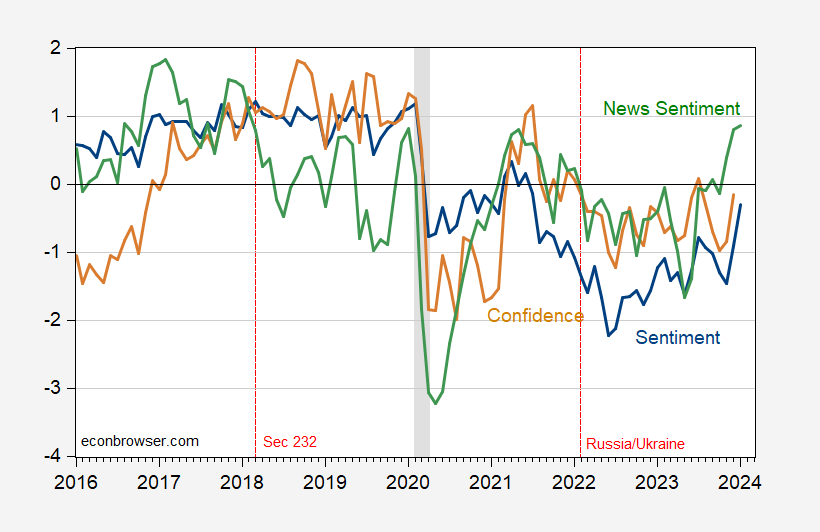

What about different indicators of sentiment? The SF Fed Information Sentiment index is a textual content based mostly indicator. In Determine 2, I present (demeaned, normalized by customary deviation) UMCSENT, the Convention Board’s Confidence Index, and the Information Sentiment Index.

Determine 2: College of Michigan Client Sentiment (blue), Convention Board Client Confidence (tan), and Shapiro, Sudhof and Wilson (2020) Day by day Information Sentiment Index (inexperienced), all demeaned and normalized by customary deviation (for the displayed pattern interval). Michigan December remark is preliminary. The Information Index remark for December is thru 1/7/2024. NBER outlined peak-to-trough recession dates shaded grey. Supply: U.Mich through FRED, Convention Board through Investing.com, SF Fed, NBER, and creator’s calculations.

Whereas the Michigan Sentiment index tracks the information index, there’s a partisan divide. Over this pattern interval, the adjusted R2 of a regression of Democratic sentiment on the information index yields is about 0.35. The analogous regression utilizing Republican sentiment has an adjusted R2 of 0.04. (A regression of the Confidence Board’s Index of Client Confidence on information sentiment has an adjusted R2 of 0.19). So primarily not one of the Republican sentiment is defined statistically by text-based information sentiment. That is per both Republican sentiment being impervious to financial data, or Republicans interpret financial information in a unique style than Democrats (or Independents, for whom the adjusted R2 is 0.19).

Extra on the partisan divide in sentiment, right here.

[ad_2]

Source_link