[ad_1]

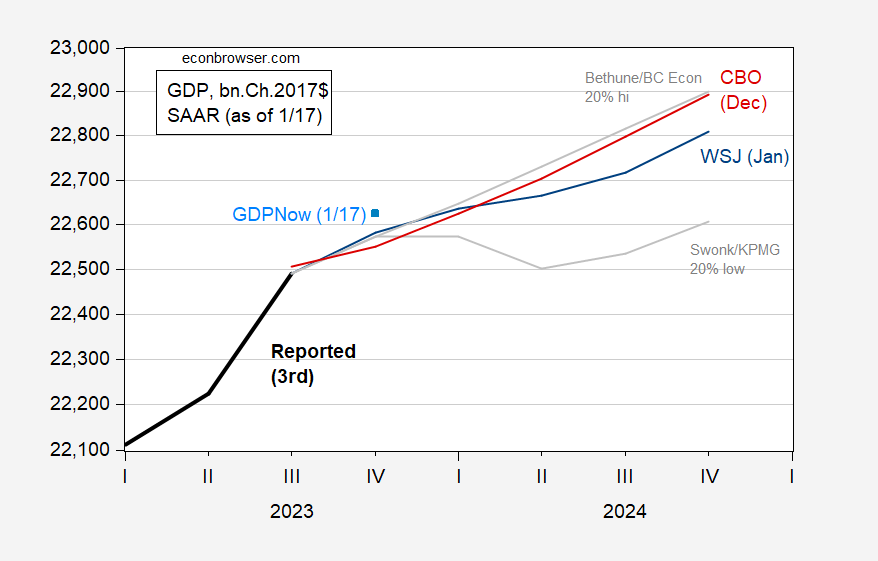

The imply forecast trajectory retains on rising as precise GDP outcomes carry on stunning on the upside (This fall imply progress rose from 0.9% to 1.7% q/q AR since October), however forecasts are fairly dispersed, as proven in Determine 1.

Determine 1: GDP (black), Imply forecast GDP from January 2024 WSJ survey (blue), 20% trimmed excessive (for 2023 this autumn/this autumn) of Bethune/Boston Faculty Economics. (grey), trimmed low of Swonk/KPMB (grey), CBO projection from December (pink), GDPNow nowcast of 1/17 (mild blue sq.), all in bn.Ch.2017$ SAAR. Supply: BEA, WSJ surveys (numerous), CBO, and writer’s calculations.

Neither imply nor median responses point out a two quarter slowdown. Nonetheless, the 20% band low entry (for this autumn/this autumn 2024) from Diane Swonk (KPMG) signifies a 0% progress in Q1, and -1.30% q/q AR in Q2. About 22% of respondents predict two or extra consecutive quarters of detrimental progress.

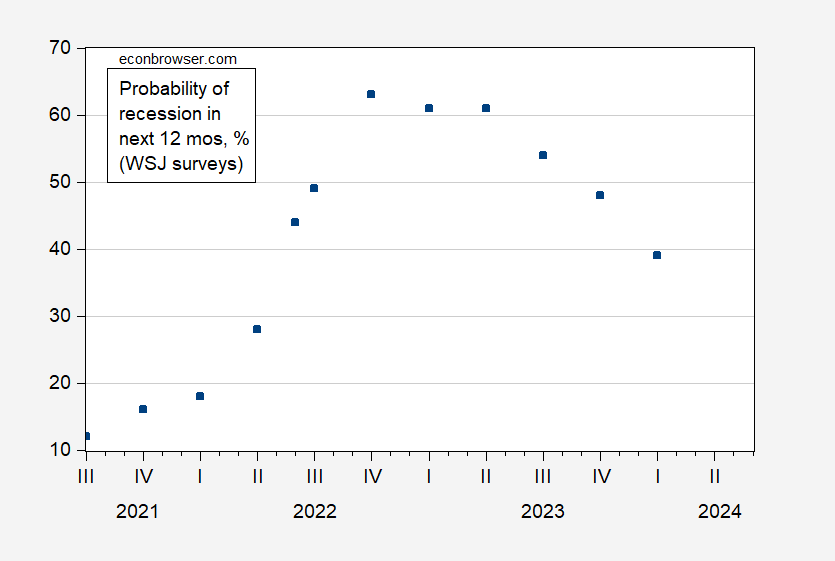

Recession likelihood declines once more.

Determine 2: Chance of recession within the subsequent twelve months. Supply: WSJ survey, numerous points.

[ad_2]

Source_link