[ad_1]

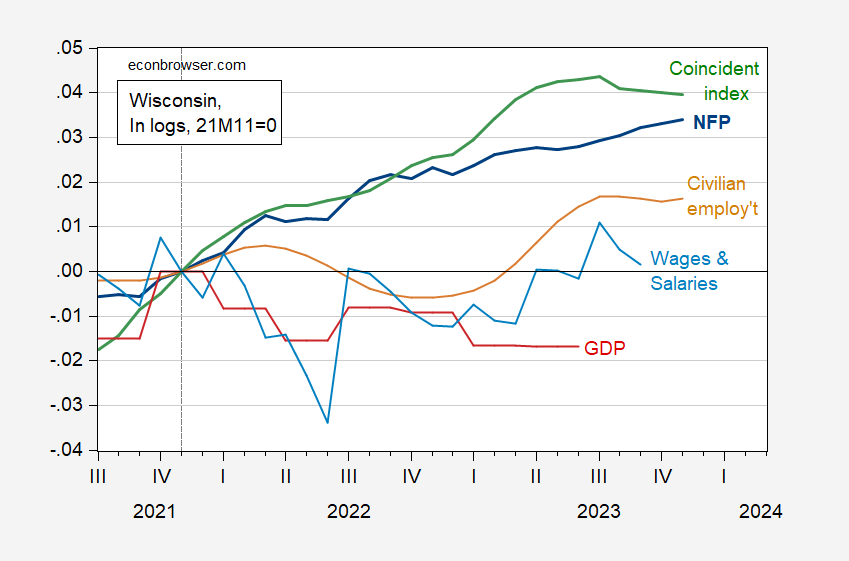

The labor market seems stronger than GDP.

Determine 1: Wisconsin Nonfarm Payroll Employment (darkish blue), Civilian Employment (tan), actual wages and salaries, deflated by nationwide chained CPI (tan), GDP (pink), coincident index (inexperienced), all in logs 2021M11=0. Supply: BLS, BEA, Philadelphia Fed, and creator’s calculations

Addendum, 12/31/2023:

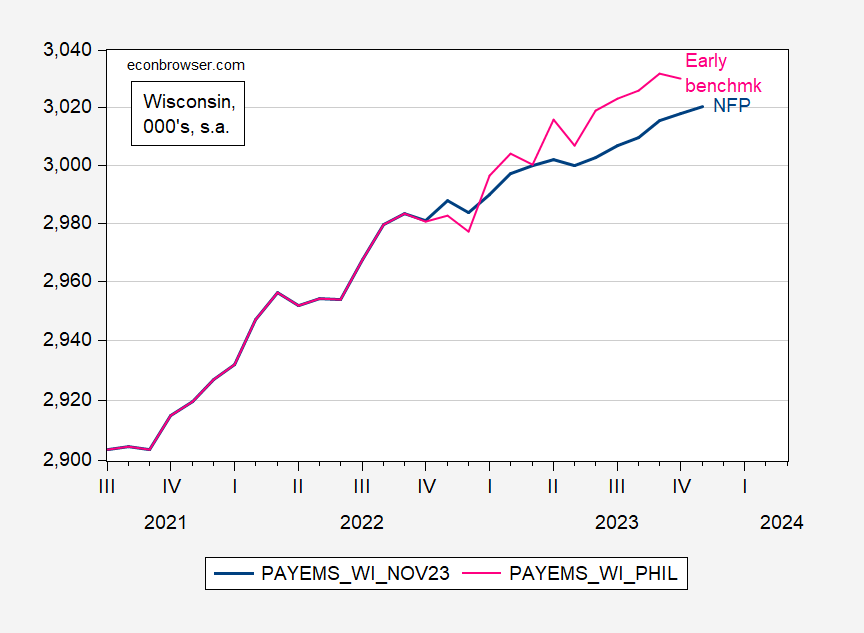

A number of questions come up from this survey. First, why is there such a divergence in measured circumstances? One factor to grasp is that sometimes labor market indicators are measured with better accuracy and timeliness than different indicators. Specifically, nonfarm payroll employment is extra dependable, much more so on the state degree than on the nationwide degree. That being stated, as tax and unemployment insurance coverage info is available in, one can get a greater repair on NFP. The Philadelphia Fed does this in its early benchmark (newest launch December 14). Utilizing this collection will increase the hole. Right here’re the official and early benchmark collection plotted.

Determine 2: Wisconsin Nonfarm Payroll Employment (darkish blue), and Philadelphia Fed early benchmark NFP (pink). Supply: BLS, Philadelphia Fed.

For October, official NFP is 0.4 ppts under early benchmark.

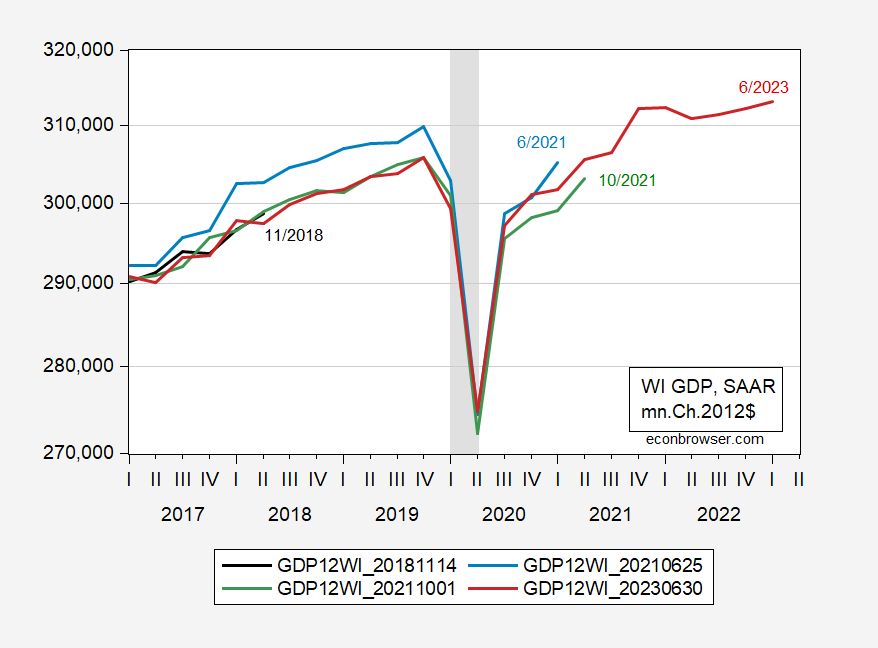

The divergence would possibly come up due to better mismeasurement of GDP. There are substantial revisions over time. Beneath is Wisconsin GDP:

Determine 3: Wisconsin GDP, classic 11/14/2018 (black), classic 6/25/2021 (blue), classic 10/01/2021 (inexperienced), 6/30/2023 (pink), mn Ch.2023$, SAAR. NBER outlined recession dates shaded grey. Supply: BEA through ALFRED, NBER.

It could be that GDP can be revised over time, thereby making the collection extra coherent.

[ad_2]

Source_link