[ad_1]

That’s the title of at present’s section on WPR’s Central Time, the place I used to be the Dean Knetter’s visitor. For my part, the rationale why the financial system has proved so sturdy to date is largely attributable to the resilience of the buyer, buoyed by Covid period switch funds. With the trail of disposable earnings increased than thought only a month in the past, consumption has been increased, and — with the saving price decrease within the context of a decent labor market — the cushion of “extra financial savings” bigger.

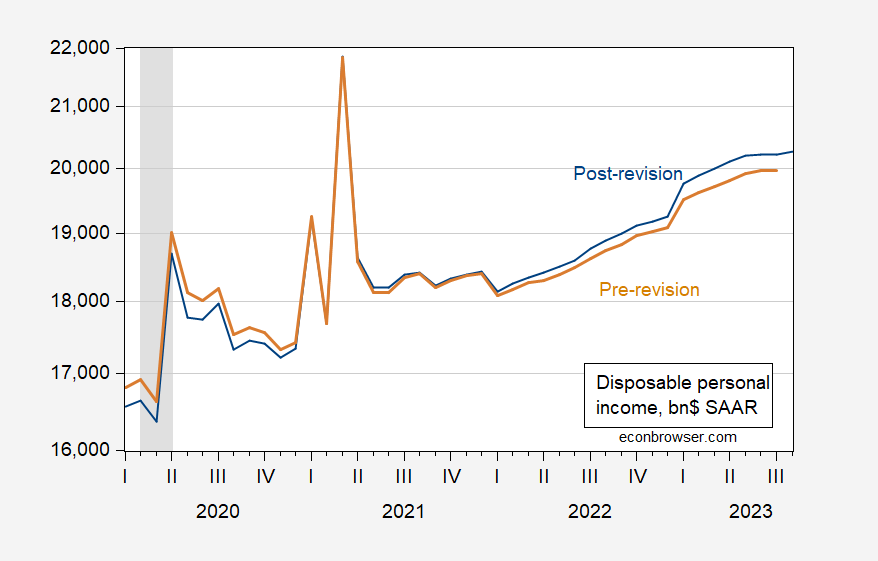

Determine 1: Pre-comprehensive revision disposable earnings (tan), post-comprehensive revision (blue), in billions $, SAAR. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA by way of ALFRED, NBER.

Wells Fargo estimates “extra financial savings” at about $1.1 trillion in August utilizing post-revision knowledge, in comparison with about $340 billion in July, utilizing pre-revision knowledge. How can this be when the cumulative distinction in disposable earnings is about $153 billion, and the cumulative distinction in consumption is $453 billion (i.e., post-revision, consumption has been a lot increased)? The distinction arises from the decrease assumed saving price (7.2% vs. prior 9.1%), which defines downward the “regular” degree of financial savings, and therefore upward the extent of “extra financial savings”. [update 10/25: for additional analysis, see Jan Groen’s substack post on the implications for “excess savings” in the 9/29 release; see also my June discussion of “excess savings” using pre-revision data]

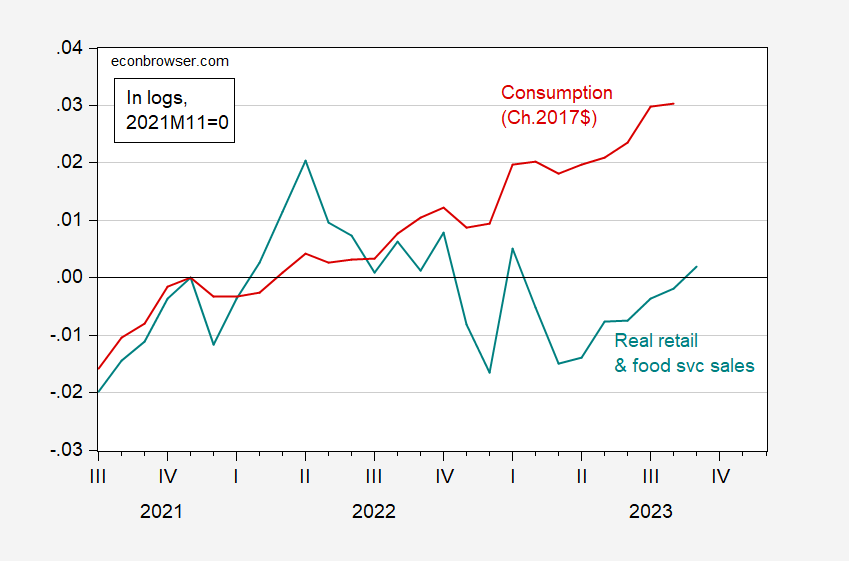

So, continued power in consumption isn’t a surprise.

Determine 2: Actual retail and meals service gross sales (teal), and actual consumption (crimson), each in logs, 2021M11=0. Retail and meals service gross sales (FRED sequence RSAFS) deflated by Chained CPI (seasonally adjusted by X13). Supply: Census, BLS, BEA and creator’s calculations.

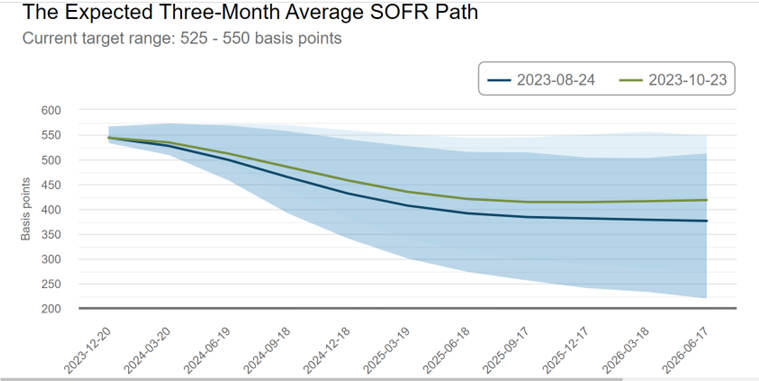

Because the resilience of the financial system has proven up time and again, and the date of a posited recession will get pushed additional again – or cancelled (see this put up) – the Fed funds path will get pushed additional up. See the trail pre-comprehensive GDP revision vs. put up, in Determine 3 under.

Determine 3: Implied path of Fed funds, from Atlanta Ate up 8/24 (blue) and 10/23 (inexperienced). Supply: Atlanta Fed chance tracker, accessed 10/24.

[ad_2]

Source_link