MBW Reacts is a collection of analytical commentaries from Music Enterprise Worldwide written in response to main current leisure occasions or information tales. MBW Reacts is supported by JKBX, a expertise platform that provides customers entry to music royalties as an asset class.

Music rightsholders waited greater than a decade for streaming worth rises. Now, lastly, the practice has left the station.

In July, Spotify introduced that it was bumping up its customary particular person Premium costs by 10% within the US – and by various quantities in 52 different markets.

In the meantime, two different distinguished music streamers – Apple Music and Deezer – each pushed up their customary particular person US costs in October final yr, from $9.99 to $10.99 per 30 days.

Doesn’t time fly?

These October 2022 streamer worth rises at the moment are very near being a full yr previous.

In MBW’s view, with inflation nonetheless snapping on the {industry}’s worth, extra, repeated streaming worth rises are already changing into inevitable.

Not solely that, however we anticipate them to reach sooner relatively than later.

Right here’s why.

voices are rising louder…

A part of the explanation MBW’s expects additional streaming costs rises are coming – whilst quickly as This fall this yr – is as a result of music’s leaders have began loudly and particularly calling for simply that.

Since Kyncl joined WMG in January, he has publicly talked about his need for streaming costs to rise (and rise and rise) a number of occasions.

In Might, on WMG’s Q2 earnings name, Kyncl stated: “Current worth will increase have been profitable and are a transfer in the correct course, however they need to be simply step one.”

Credit score: Warner/press

“We consider the market will bear additional [streaming] worth will increase sooner or later, and we’re anticipating that they’ll arrive on a extra common cadence than previously.”

Having praised the likes of Spotify, Apple, Amazon, Deezer, and TIDAL for upping their costs, Kyncl stated: “We see these preliminary worth will increase as an encouraging begin. There is no such thing as a proof that the companies are experiencing elevated ranges of churn.

“We consider the market will bear additional worth will increase sooner or later, and we’re anticipating that they’ll arrive on a extra common cadence than previously.”

Others indicating their needs for a similar final result have included Kyncl’s two fellow main music firm bosses – Rob Stringer at Sony Music Group, and Sir Lucian Grainge at Common Music Group – in addition to Invoice Ackman, shareholder of Common Music Group by way of Pershing Sq. Holdings.

Credit score: Kristoffer Tripplaar / Alamy

“We consider that breaking the $10 barrier is a watershed second, as different platforms will possible observe swimsuit, and common worth will increase will develop into the norm within the audio streaming {industry} as they’re within the video streaming {industry}.”

Invoice Ackman / Pershing Sq., March 2023

Way back to March 2023, Ackman celebrated the current worth rises at Apple Music and Amazon Music and many others. by noting in a Pershing Sq. investor replace: “We consider that breaking the $10 barrier is a watershed second, as different platforms will possible observe swimsuit, and common worth will increase will develop into the norm within the audio streaming {industry} as they’re within the video streaming {industry}.”

Additionally, don’t neglect that in June, Goldman Sachspredicted that common streaming subscription costs in developed markets just like the US would develop, on common, by 3% per yr within the medium-term future.

Now, the remainder of us can see exhausting proof of why main gamers in music assume the market can bear additional worth rises – and shortly – because of the newest stats from the Recording Trade Affiliation of America (RIAA).

After the worth rises, premium ARPU jumped within the US – with no decline in subscribers. (Additionally, new subs are getting tougher to return by…)

The optimistic influence on Premium streaming ARPU from various the aforementioned worth rises within the US market (specifically: Apple Music, Amazon Music, Deezer, and an October 2022 rise in Household Plan pricing on YouTube Music) was very obvious within the H1 2023 figures from the RIAA, as issued earlier this week.

What was additionally obvious, nevertheless, was the explanation main music firms could now develop even much less affected person to see further worth rises within the US: A slowdown within the progress of subscription volumes.

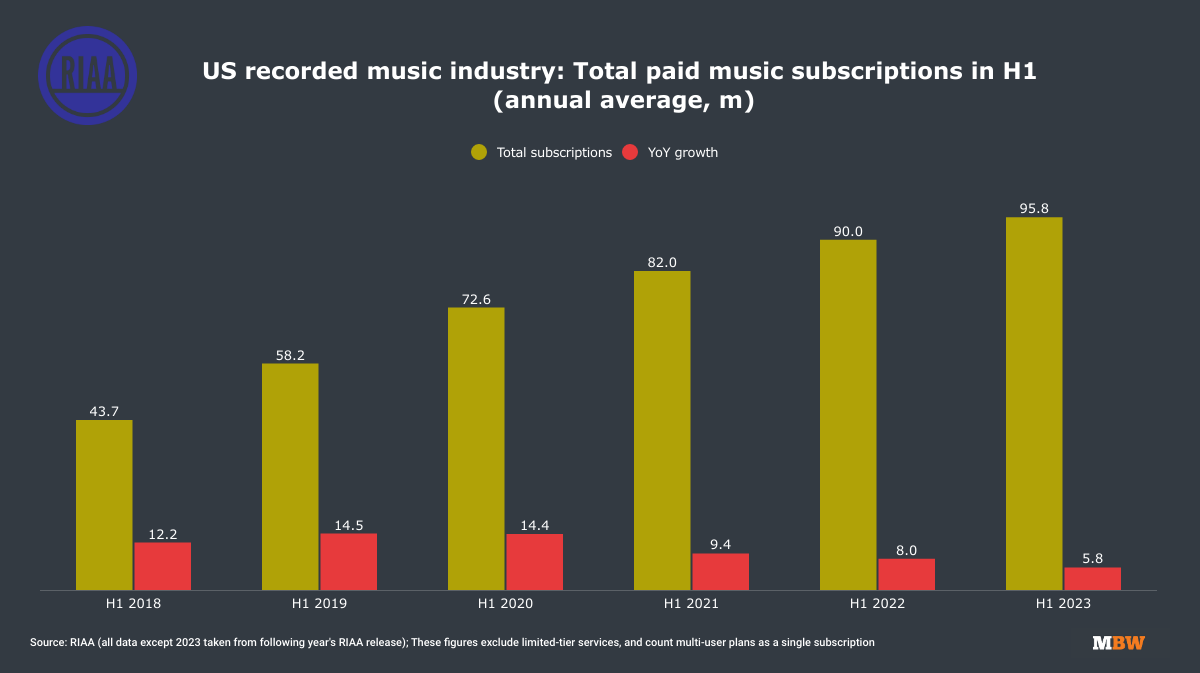

In H1 2023, on common, there have been 95.8 million subscribers to full ‘paid’ subscription companies in the US, in accordance with the RIAA.

That quantity, although, was up by simply +5.8 million subscribers year-on-year (versus the equal interval in 2022).

And that +5.8m determine, in flip, was considerably smaller than the YoY progress we’ve seen in the US lately (see crimson bars under).

Conclusion?

There can now be little doubt – judging by the chart above – that an inevitable decline within the variety of new music subscribers out there in the US is underway.

For that motive, the {industry}’s consideration will now certainly change extra readily to bettering the ARPPU (Common Income Per Premium Consumer) of the prevailing subscribers it already counts on this planet’s greatest music market.

And the simplest strategy to bump that ARPPU determine is, in fact… worth rises.

Certainly, this state of affairs is already enjoying out within the US.

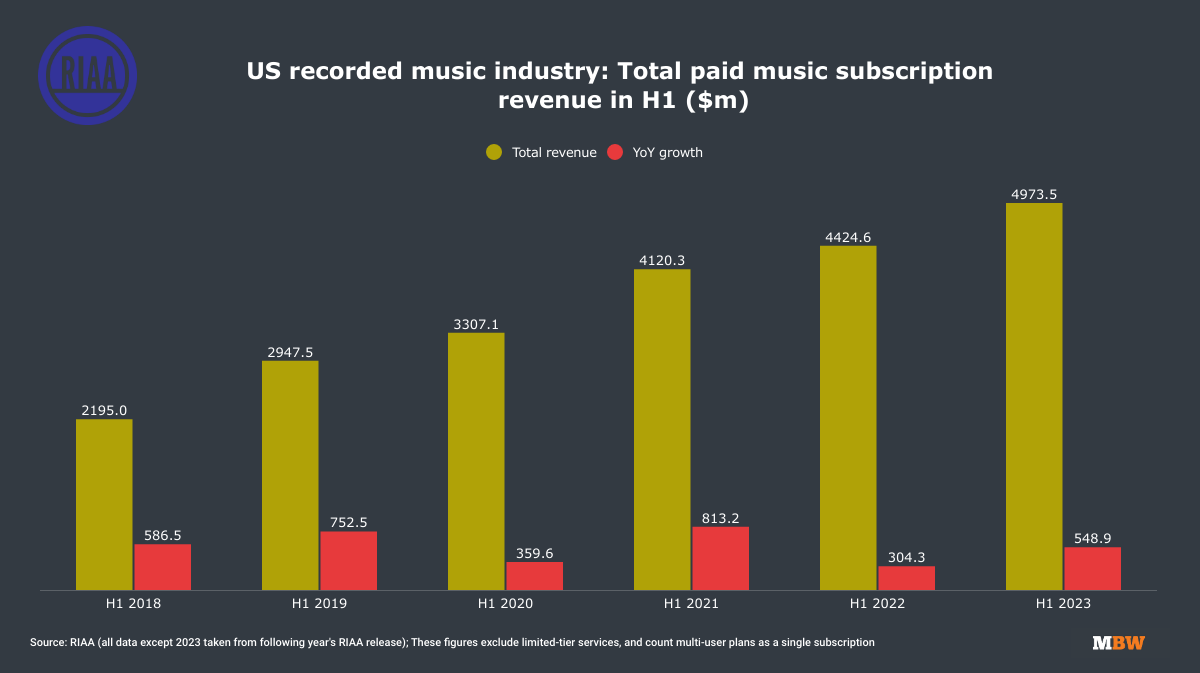

The RIAA’s newest figures might need proven a decline in YoY streaming subscriber quantity progress within the US – however they really confirmed an acceleration within the quantity of cash being generated for the recorded music enterprise by ‘paid’ streaming subs.

Not together with ‘limited-tier’ companies, the commerce income from Premium streaming companies within the US in H1 2023 hit USD $4.973 billion, up by $548.9 million YoY.

Within the equal year-ago interval (H1 2022), those self same Premium streaming revenues had been up by simply $304.3 million YoY.

The most important issue on this improved progress may have been a rise in streaming costs at Apple Music, Amazon Music et al that boosted the H1 2023 ‘Paid’ subscription income numbers.

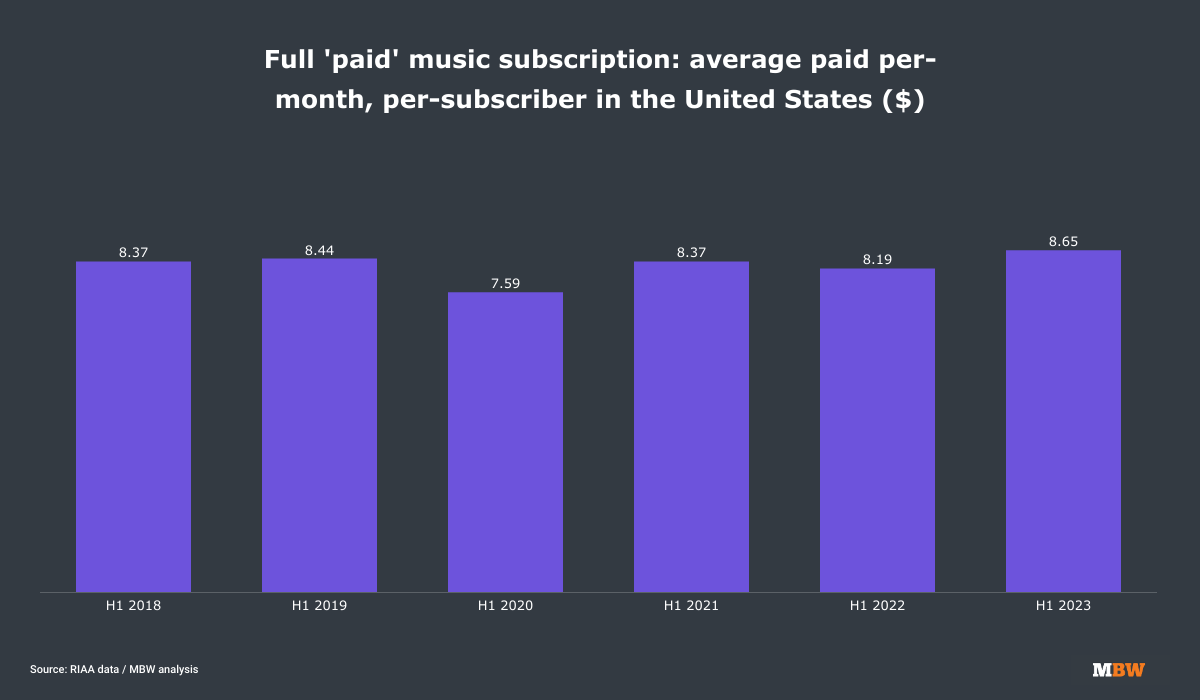

To see exactly how useful this was to the music {industry}, under MBW has discovered how the RIAA’s H1 ‘Paid’ streaming figures labored out as a month-to-month ARPPU.

(The chart beneath reveals the results of dividing the RIAA’s H1 determine for ‘paid’ streaming income by its common H1 subscriber quantity determine – after which dividing once more by six months.)

Calculations made utilizing RIAA’s ‘Paid’ subscription income, not together with ‘limited-tier’ companies

Be aware that the common month-to-month ARPPU of a US ‘paid’ streaming subscriber rose by 46 Cents per head YoY in H1 2023 (to $8.65) – and these numbers weren’t even boosted by Spotify’s worth rise (which got here in July 2023, aka H2 2023).

(If the numbers within the chart above appear excessive, keep in mind that the RIAA’s ‘Paid’ subscriber quantity determine counts multi-user plans as a single subscription. So a $16.99 Apple Music household plan, for instance, would depend as one sub.)

Does a 46 Cent rise in month-to-month ARPPU seem to be small potatoes to you?

Then we humbly counsel you do the maths: Throughout 95.8 million subscribers, that 46 Cents per 30 days bump equates to an industry-wide enhance of $44 million per 30 days… or $528.8 million per yr, for streaming commerce income.

Music rightsholders in all places are going to wish to see increasingly ARPPU bumps like that they loved in H1 2023 – and meaning extra streaming worth rises.

Don’t anticipate to attend too lengthy for them to get what they’re demanding.